Executive Summary

- Since the end of February, the conflict between the USA, Israel, and Iran has been escalating. Attacks on energy facilities and the blockade of the Strait of Hormuz are leading to massive oil and gas shortages on the world market.

- Energy shortages are slowing growth and driving inflation. Growth forecasts are being revised downward.

- Government bond yields are rising sharply as markets expect higher inflation and short-term interest rate hikes. Central banks are keeping their key interest rates stable for now, but are signaling a possible tightening – the first step is already coming from Australia.

- Rising risk premiums tend to burden stock markets, while political uncertainties in the US are also causing unrest.

- Moderate US inflation data in the second half of the year open up room for further interest rate cuts in the medium term.

- The war in the Arabian Gulf has led to a disruption of energy supply chains and price surges for oil and gas. Inflation prospects have increased, which bond markets are pricing in with higher yields.

- Nervousness has noticeably increased in the stock markets due to the escalation in the Middle East.

- The US dollar is seen as a safe investment amid geopolitical turmoil and is trading higher. The Swiss franc also remains strong and benefits from increased uncertainty.

- Gold corrects, despite or because of the instability in the Gulf.

Our macroeconomic assessment

Business cycle

- Since February 28th, the US and Israel have been bombing Iran. The Mullah regime is striking back against Israel and US-allied Gulf states. The military strikes are hitting the Iranian leadership as well as infrastructure throughout the region. As a means of pressure, Iran is blocking the Strait of Hormuz. This is causing the largest oil and natural gas supply shortage. Global energy prices are exploding.

- Missing energy resources and reduced food production due to the absence of nitrogen and phosphate fertilizers on the world market threaten to curb global economic growth and fuel inflation.

- Given the uncertainties, supply bottlenecks, and higher prices, we are lowering our forecasts for the current year globally to 2.9%, for China to 4.4%, for the EU and Switzerland to 1%, and for the UK to 0.9%. For now, we are maintaining our forecast for the US at 2%.

- Due to current events in the Middle East, the trade dispute of the US administration, the decision of the US Supreme Court against illegally levied tariffs, and new alternative levies are fading into the background.

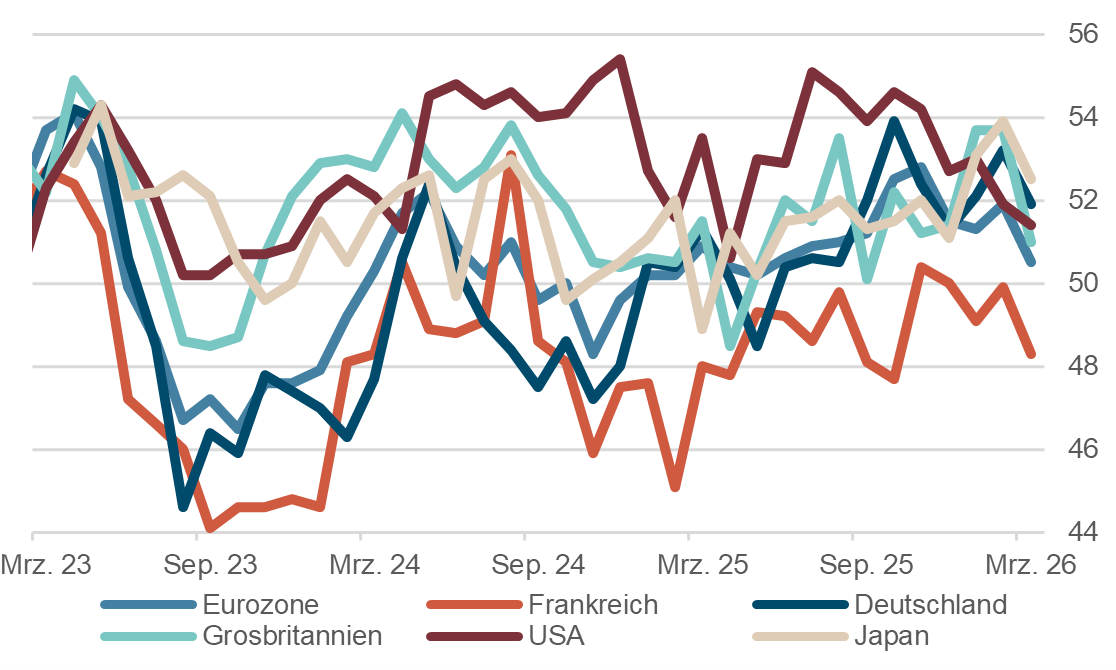

March Purchasing Managers' Indexes Under Pressure

Source: Bloomberg Finance L.P.

Monetary policy

- The military strikes against energy infrastructure are driving energy prices and thus the commodity index tracked by Bloomberg to levels not seen since the aftermath of the Corona pandemic.

- As long as supply bottlenecks persist in the energy sector, sustained inflationary pressure must be expected. This, in turn, increases the probability of a stagflation scenario.

- Yields on government bonds are reacting noticeably to the tense geopolitical situation and the looming inflation surge. This should also bring the discussion about a structural cycle of rising yields into investors' focus.

- For the coming quarters, central bankers expect inflation to pick up due to rising energy prices and no longer rule out tightening their monetary policy.

Our investment policy conclusions

Bonds

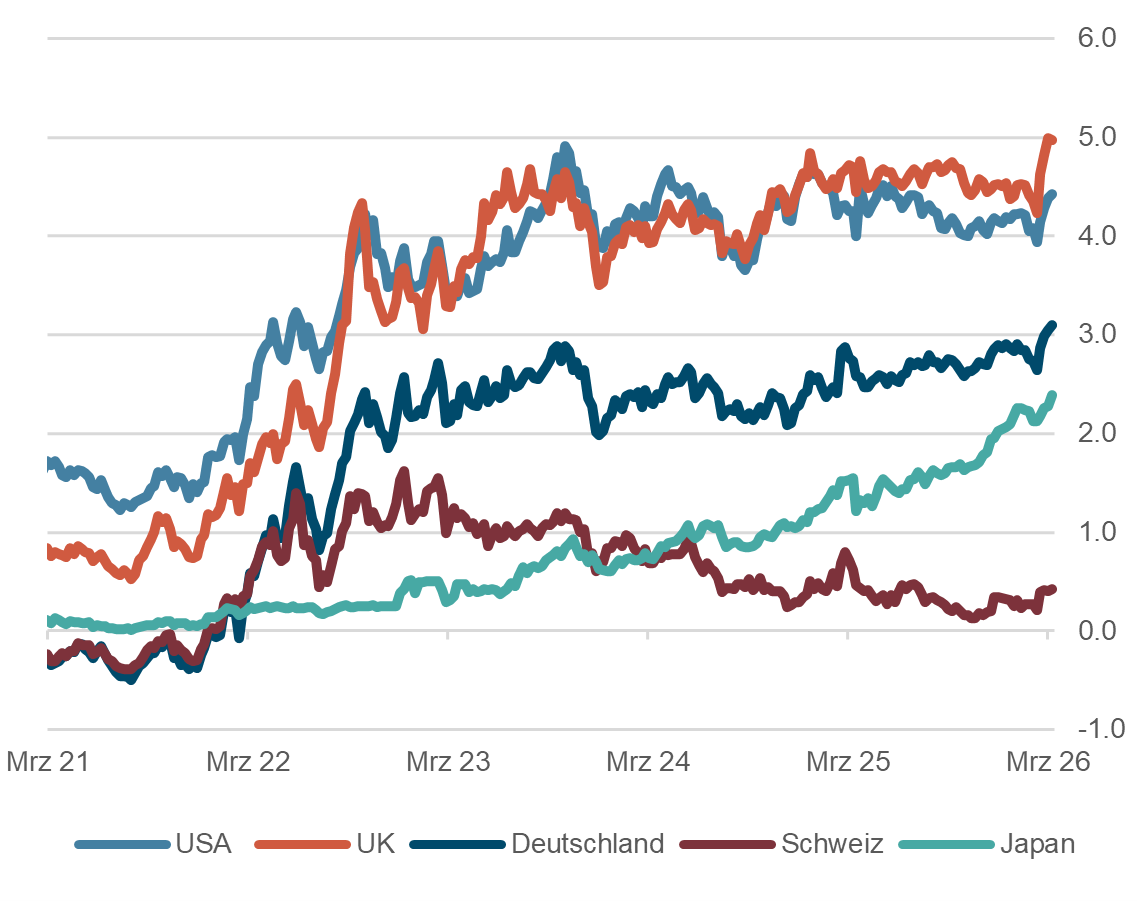

- Currently, yields on 10-year government bonds stand at around 4.41% in the U.S., 3.11% in Germany, 0.41% in Switzerland, and 2.41% in Japan.

- The crisis in the Middle East initially had a dampening effect on government bond yields, as it led to increased demand for safe assets, particularly so-called «safe havens» like Swiss government bonds.

- However, price surges for oil and gas, caused by disruptions in energy supply chains, have led to a rise in yields. Consequently, yields in the most important regions are higher today than before the outbreak of the war.

- The recent wave of difficulties in the private credit sector has brought risks back into public awareness and is having a spillover effect on corporate bond and high-yield spreads.

Interest on 10-year government bonds, in %, 5 years

Source: Bloomberg Finance L.P.

Equities

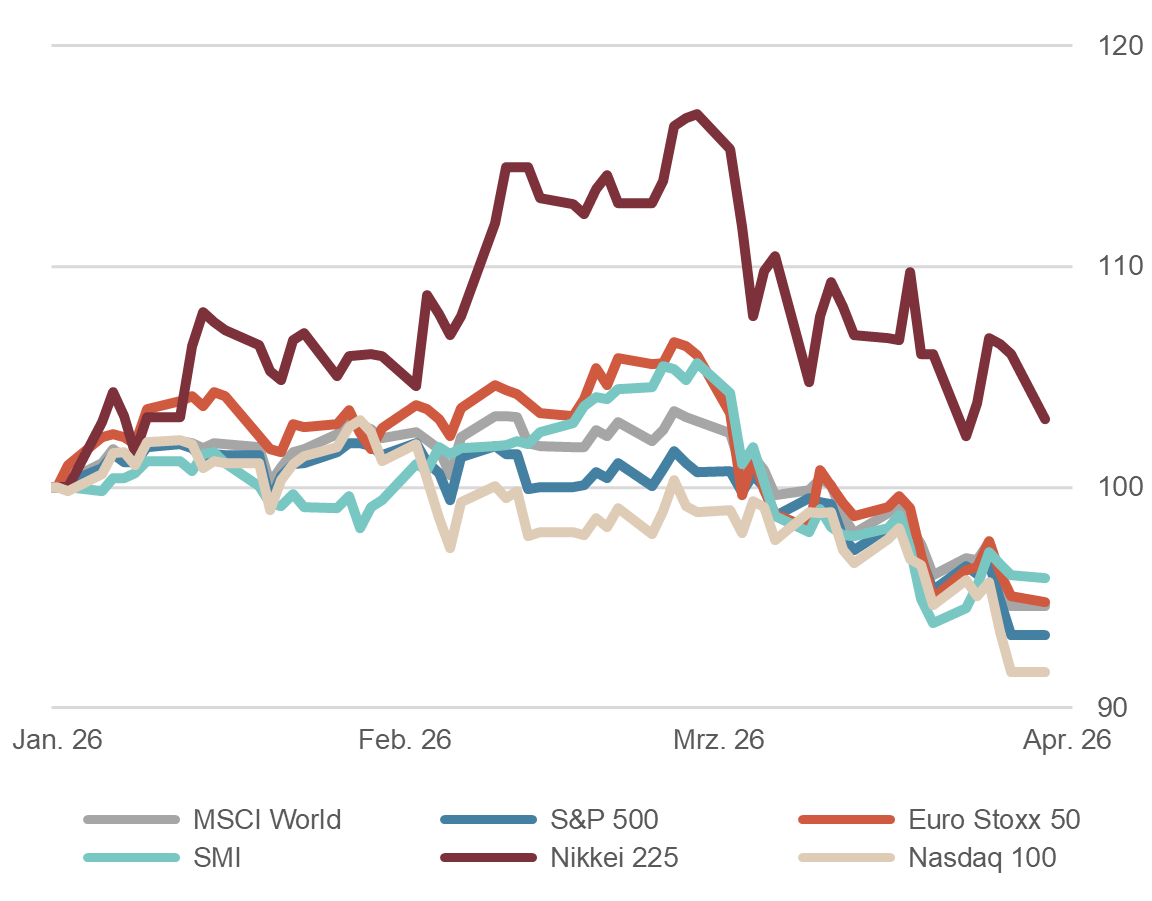

- Nervousness on the stock markets has risen noticeably due to the escalation in the Middle East. As a result, after a positive start to the year, the indices have fallen significantly. Both the Nasdaq and the S&P 500 are now down about 10% from their highs.

- Stock markets in Europe are showing some weakness, which also corresponds to a historical pattern in geopolitical crises. The SMI, DAX, and EuroStoxx are losing significantly – only the FTSE 100 is performing slightly better.

- It will be crucial how long the uncertainty due to the crisis in the Middle East and the resulting disruptions to international supply chains lasts. Stock markets fear similar braking effects on the global economy as were triggered by the Covid pandemic at the time. Conversely, a swift resolution of the war would likely trigger a strong rally, as robust corporate earnings are still expected.

Equity markets, performance year to date, indexed

Source: Bloomberg Finance L.P.

Forex

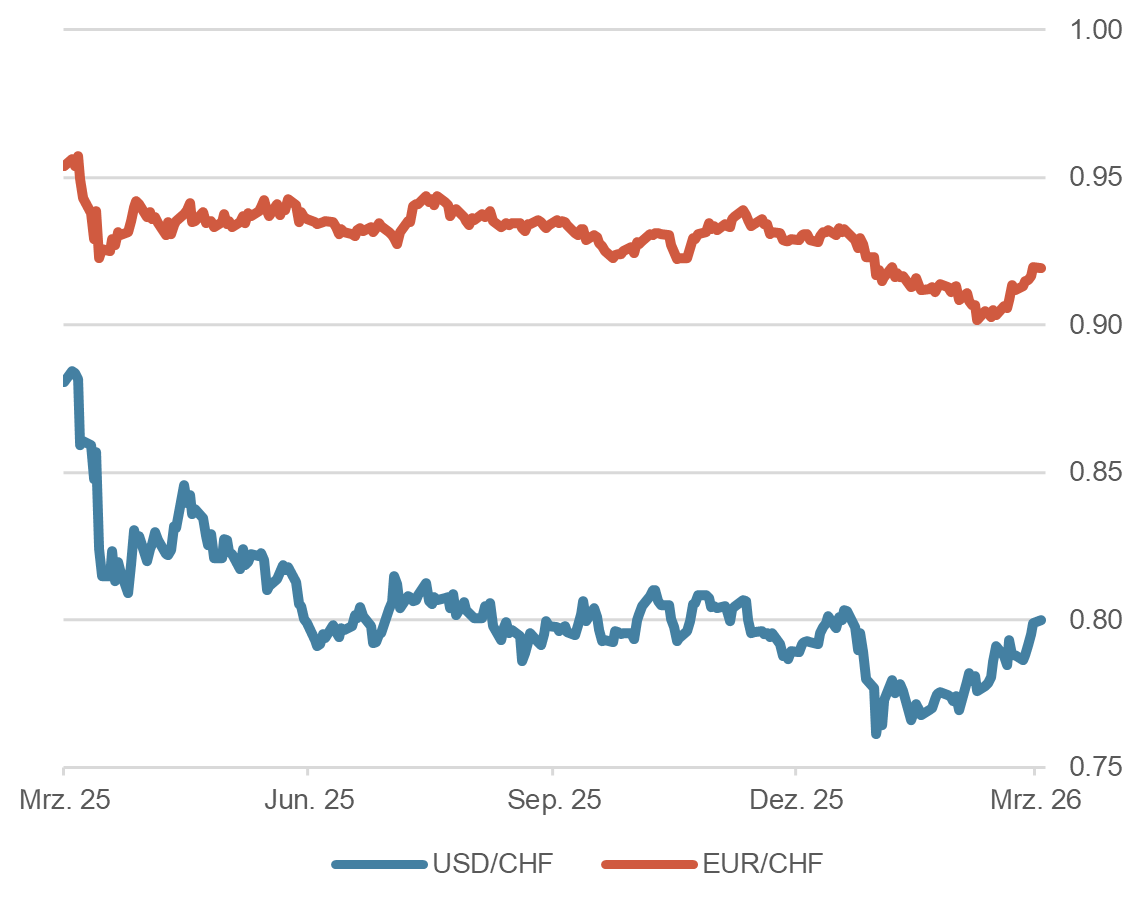

- The US dollar has reacted to the escalation in the Middle East as it typically does in geopolitical crises: it tends to strengthen. Against the Swiss franc, it advanced to around 0.80. However, the appreciation against other currencies has been even stronger, as the CHF also fulfills its role as a safe-haven currency in such market phases.

- The EUR/CHF also moved slightly higher and is currently trading around 0.92. We consider the level around 0.90 to be solid support, not least due to the SNB's recent statement that it would not lower key interest rates below zero if possible, but rather combat any further franc strength through foreign exchange market interventions.

- Overall, the Swiss franc remains strong across the board and continues to benefit from Switzerland's «safe haven» status amidst ongoing geopolitical uncertainty and the fiscal indiscipline of many other countries and economic areas.

Dollar and euro against franc, 1 year

Source: Bloomberg Finance L.P.

Disclaimer: Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no undertaking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information provided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other transaction. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.

Disclaimer: Produced by Investment Center Aquila Ltd.

Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no under-taking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information pro-vided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other trans

action. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.