This website uses cookies. For more information about this and your rights as a user, please see our Privacy policy.

To use our website, you must accept our privacy policy.

The US intervention in Venezuela marks a geopolitical turning point and the first concrete implementation of the updated US doctrine in the Western hemisphere. The overthrow of Maduro is less an isolated military action than a strategic demonstration of power vis-à-vis China, Russia and Iran. Chinese investments in the oil sector have been effectively devalued and control over Venezuela's resources now lies with the USA.

Despite considerable reserves, high investment costs, institutional weaknesses and fragile stability remain key risks. We are not making any immediate tactical adjustments, but see our strategic orientation confirmed. Gold remains overweight as insurance against geopolitical escalation, inflation risks and fiscal indiscipline, while we continue to underweight traditional bonds and consistently hedge in CHF.

The event

What happened?

In the early hours of January 3, 2026, US forces launched targeted attacks on the Venezuelan capital Caracas in a wide-ranging military operation. Numerous explosions rocked the city, including attacks on military installations such as the La Carlota air base and anti-aircraft defense systems. The declared main objective: the arrest of President Nicolás Maduro.

Special forces, who were already involved in the killing of Osama bin Laden, broke into the presidential palace, arrested Maduro and his wife Cilia Flores and flew them both to a US warship in the Caribbean. From there they were transferred to New York, where they are being held in the Metropolitan Detention Center.

According to official information, the operation lasted less than three hours and met with no significant resistance from the Venezuelan armed forces. It took place against the backdrop of months of political tensions between Washington and Caracas, which had recently intensified significantly. According to the US government, the operation was also based on "concrete security findings" that made immediate intervention necessary.

The Venezuelan government described the action as an "illegal invasion" and spoke of a serious breach of international law.

On 4 January, the US Department of Justice immediately brought charges against Maduro and five other individuals for their alleged roles in a drug trafficking network and for collaborating with groups that the US classifies as foreign terrorist organizations. Maduro has vehemently denied these accusations before and now also in the indictment.

Voices from official sites

Following the military operation in Venezuela, representatives of the US government and international players used some drastic words. US President Donald Trump repeatedly described the operation as an extraordinary success. At a press conference, he said: "This was one of the most impressive, effective and powerful military actions by the United States." Trump described the operation as an "attack the likes of which have not been seen since World War II" and announced: "We will remain in the country until a safe, orderly and responsible transition is possible."

Trump also announced economic ambitions in Venezuela: "Our very large US oil companies, the largest in the world, will invest there, spend billions, repair the broken infrastructure and start making money for the country."

Defense Minister Pete Hegseth explained that the operation was the result of months of planning. He said of Maduro: "He had his chance, just as Iran had its chance. But then it was over. He overdid it and suffered the consequences."

General Dan Caine, Chairman of the Joint Chiefs of Staff, explained the operation, codenamed "Operation Absolute Resolve": "The operation was discreet, precise and carried out in the darkest hours of January 2nd. It was the result of months of planning and preparation. An operation that only the US military can carry out."

The declared war on drug trafficking

A central motive of the US government for its intervention is the accusation that Venezuela, along with other South American states, is an active part of the international drug trade under Nicolás Maduro.

The Venezuelan opposition leader María Corina Machado painted a similarly gloomy picture. At a press conference in Norway 2025, she said: "Some people are talking about an invasion of Venezuela. My answer is that this has already happened. Russian agents, Iranian agents, terrorist groups such as Hezbollah and Hamas operate freely according to the regime's instructions. Colombian guerrillas and drug cartels control sixty percent of our population. It's not just about drugs, but also about human trafficking and prostitution. Venezuela has become the criminal center of the Americas."

These statements underscore the narrative that Venezuela is no longer perceived merely as an authoritarian regime, but as a transnational criminal network with a direct impact on US security.

Trump explicitly positioned the operation in Venezuela as part of a broader security policy strategy. He also referred to historical US doctrines: "The Monroe Doctrine was important, but we've gone much further. Some now call it the 'Donroe Doctrine', but I don't know exactly."

The statements show that the US government under Trump is not just looking at Venezuela. He went on to say in a press conference: "[Colombian President] Petro is producing cocaine that is coming into the United States, so he better watch himself." When asked by a reporter whether an operation against Colombia was imminent, Trump replied: "Sounds good to me." Mexico was also sharply criticized: "Something has to be done with Mexico, too. It's not ruled by a president, it's ruled by cartels."

Foreign Minister Marco Rubio also emphasized the strategic importance of the action: "This is the Western Hemisphere. We will not allow our adversaries to establish a base of operations here ... This is over." With regard to Cuba, he added: "If I were part of the Cuban leadership, I would be very worried right now."

Maduro's arrest is therefore seen as a signal in Washington: The fight against organized crime is being waged militarily and Latin America is under observation. A return to the previous restraint does not appear to be planned.

The "Donroe Doctrine": a new era of American dominance in the Western Hemisphere?

In the United States National Security Strategy of November 2025, the US government announced a fundamental realignment of its foreign and security policy in the Western Hemisphere. Building on the historic Monroe Doctrine, the document formulates a modernized guideline known as the "Trump Corollary to the Monroe Doctrine" and, as mentioned, is also referred to by critics and supporters as the "Donroe Doctrine".

The aim is to restore and secure the supremacy of the USA in the western hemisphere. It reads: "After years of neglect, America will reassert and enforce the Monroe Doctrine to restore American supremacy in the Western Hemisphere."

Among other things, the strategy envisages denying non-hemispheric competitors - primarily China, Russia and Iran - access to critical resources, military presence or infrastructure in the American sphere of influence. According to the strategy, the US claims the right to prevent foreign influence by any means necessary: "We want other states to view us as a preferred partner and we will (in various ways) discourage their cooperation with others."

It also calls on Latin American governments to cooperate more closely with the US, particularly in the fight against drug cartels, transnational crime and migration. It also states that the hemisphere should be free from "hostile foreign influence or ownership of strategic assets", instead supporting critical supply chains and securing US access to key regions.

The "Donroe Doctrine" therefore represents a geopolitical clarification: The USA claims the western hemisphere as its own security policy area and is prepared to secure this position militarily and economically. The operation in Venezuela can therefore be interpreted as the first concrete implementation of this new strategic line.

However, this is not just about domestic political stabilization or the fight against organized crime. At its heart is also a geopolitical trial of strength with China. After all, the operation in Venezuela not only removed an authoritarian regime from power, but also cut one of Beijing's most important energy connections in the western hemisphere.

China's investments in Venezuela

China has invested heavily in Venezuela over the past two decades, primarily through oil-backed loans. Between 2007 and 2015, Beijing provided the country with more than 60 billion US dollars in financing: Money that Caracas was supposed to pay back to China with long-term oil supply contracts. This sum was equivalent to around 16% of Venezuelan GDP and made China Venezuela's largest lender.

Without the Chinese loans, Venezuela would probably have run into payment difficulties years ago. Tens of billions are still outstanding today; estimates put the outstanding loans linked to oil at around 19 billion US dollars.

In addition to the loans, Chinese companies, mostly state-owned oil companies, had negotiated stakes in Venezuelan oil fields and long-term production agreements. It was not until 2024 that a private Chinese company, China Concord Resources Corp. (CCRC), signed a 20-year production contract to expand oil production in Venezuela.

After the forced change of power in Caracas, however, all of these deals are in danger of becoming invalid. The previously "ironclad" contractual rights of Chinese players could effectively be worthless.

The direct oil supply relationship between Venezuela and China is also on the verge of collapse. As a result of US sanctions since 2019, China has replaced the Western market as the main buyer of Venezuelan oil. Most recently, it was estimated that up to 80% of Venezuelan oil exports went to China. This corresponded to around 750,000 barrels of crude oil per day, which were purchased by Chinese importers, allowing the Maduro regime to earn a minimal amount of foreign currency. By comparison, this volume accounted for around 4% of total Chinese crude oil imports.

For China, Venezuelan oil was therefore only a small part of the import portfolio in terms of volume, but nevertheless strategically important. On the one hand, it was heavy crude oil from the Orinoco Belt, which a number of Chinese refineries are designed to process. Secondly, Venezuela's crude oil was traded at high discounts due to the sanctions, with estimates of 30% or more below market. Access to this heavily discounted heavy oil was crucial for Chinese refineries in order to secure their already tight margins.

Independent Chinese refineries in particular, known as "teapots", readily seized the opportunity, despite the sanctions risks: according to Reuters, around two thirds of China's Venezuelan oil imports ended up with these smaller refineries, which were able to process the crude oil more profitably thanks to the discounts. The remaining third of deliveries went directly to Chinese creditors as repayment for the high loans to Caracas. If the US sanctions were lifted or the oil diverted elsewhere, China would lose out twice over, as the refiners would have to switch to more expensive heavy crude oil from other sources and the repayment of the loans through oil would be in question.

In fact, the consequences of the US intervention are already becoming apparent. Immediately after the strike on Caracas, several oil tankers changed their route. According to the Wall Street Journal, the Chinese supertanker "Thousand Sunny", which was on its way to Venezuela, turned around and set course for Nigeria. Other tankers dropped anchor.

Beijing's rhetoric was correspondingly harsh: it was "deeply shocked" and condemned the "reckless use of force" by the US, the Chinese Foreign Ministry declared a few hours after the night-time explosions in Caracas. Washington's actions constituted a "serious violation of international law" and Venezuela's sovereignty, according to the accusation from Beijing.

A precedent for Taiwan?

Most current analyses contain no indication that China sees the US military action in Venezuela as carte blanche for its own violent "solution" to the Taiwan issue.

Beijing is using the incident to brand the US as a hegemonic lawbreaker. The idea of a "precedent" is also the subject of lively discussion in the Chinese online public, in some cases triumphantly as a "prime example" of an attack against Taiwan.

However, officials in Beijing clearly separate the Taiwan issue from the Venezuela event and renowned Chinese experts emphasize that an attack on Taiwan would be determined by China's own capabilities and interests, not by US interventions elsewhere.

Western security experts support this view: despite some fears of a new escalation logic, the majority opinion is that Xi Jinping's calculation remains unchanged and that he does not need (or seek) an additional reason to take action against Taiwan one day if circumstances require it from the Chinese perspective.

Nevertheless, the US deployment has crossed a symbolic threshold that is being felt globally. It provides China with "cheap ammunition" in the diplomatic dispute and could serve as a long-term argument to justify its own robust actions. For Taiwan, the episode means increased vigilance: the island republic will want to further strengthen its defense and tie itself even more closely to the USA.

But how high is the actual risk of a Chinese invasion of Taiwan? Let's follow the money: a look at the markets that allow betting on political events, such as polymarket.com, suggests that the perceived probability of a short-term escalation is rather low. For example, the implied probability of an invasion by the end of March 2026 is only 4%, rising moderately to 7% by the end of June 2026 and reaching around 13% for the tenor by the end of 2026.

Source: polymarket

So far, the attack on Venezuela has not triggered an immediate threat of war in East Asia, but the erosion of previous taboos in international politics is unmistakable and is causing tense calculations for the future on all sides.

Motivation

Ist es das Öl?

Zurück zum «schwarzen Gold»: haben es die USA auf die venezolanischen Reserven abgesehen? Auf den ersten Blick wirkt diese Annahme überraschend. Seit der sogenannten Schieferölrevolution fördern die USA heute so viel Erdöl wie nie zuvor und liegen damit deutlich über der Produktion vieler klassischer Förderländer. Venezuela hingegen ist unter der jahrzehntelangen sozialistischen Führung und den damit verbundenen amerikanischen Sanktionen der letzten Jahre zu einem der kleineren Produzenten abgestiegen. Warum also sollte Washington nun ausgerechnet an venezolanischem Öl interessiert sein?

Gemäss dem Sky-Analysten Ed Conway liegt die Antwort liegt nicht in der Menge, sondern in der Art des Öls. Rohöl ist keineswegs gleich Rohöl. Je nach geologischen Bedingungen unterscheidet man zwischen leichtem, mittlerem und schwerem Rohöl. Leichtes Öl ist dünnflüssig und relativ einfach zu verarbeiten, schweres Öl hingegen zäh, teerartig und technisch anspruchsvoller. Oft muss es erst verdünnt werden, damit es überhaupt durch Pipelines transportiert werden kann.

Genau hier liegt der entscheidende Punkt: Das durch Fracking gewonnene amerikanische Schieferöl ist überwiegend leichtes Rohöl.

Vor dem Durchbruch der Fracking-Technologie konzentrierte sich die amerikanische Ölproduktion auf konventionelle Felder, etwa in Texas, Kalifornien oder Alaska, deren Rohölqualitäten eher schwer oder mittel waren. Die grössten US-Raffinerien, insbesondere an der Golfküste in Texas und Louisiana, wurden deshalb über Jahrzehnte hinweg auf die Verarbeitung von schwerem Rohöl ausgelegt. Diese Anlagen lassen sich nicht ohne enormen finanziellen Aufwand umrüsten, falls es überhaupt möglich ist. Um Benzin, Diesel und andere Produkte in ausreichender Menge herzustellen, benötigen sie weiterhin schwere Rohölsorten, um ihre Kapazität auszulasten.

Obwohl die USA also heute mehr Öl fördern als je zuvor, sind sie weiterhin stark auf Importe angewiesen, und zwar vor allem auf schweres Rohöl. Während früher nur ein kleiner Teil der Einfuhren aus dieser besonders dichten Ölform bestand, machen schwere Sorten inzwischen den Grossteil der US-Ölimporte aus.

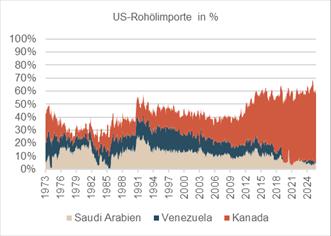

Die wichtigsten Lieferanten für dieses schwere Rohöl sind Russland, Kanada, Mexiko und potenziell Venezuela. Tatsächlich stammt heute der überwiegende Teil der US-Importe aus Kanada, während Venezuela aufgrund politischer Spannungen und Sanktionen kaum noch eine Rolle spielt.

Quelle: U.S. Energy Information Administration

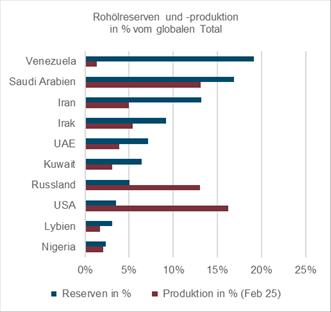

Doch gerade hier wird die strategische Dimension sichtbar. Ein Blick auf die globalen Ölreserven zeigt, warum Venezuela für die USA langfristig von Bedeutung sein könnte. Das Land verfügt über die grössten nachgewiesenen Erdölreserven der Welt, noch vor Ländern wie Saudi-Arabien, Iran oder Irak. Dabei handelt es sich grösstenteils um genau jenes schwere Öl, das amerikanische Raffinerien benötigen.

Quelle: OPEC

Die Sache mit den Zahlen

Die zugrunde liegenden Zahlen zu den Erdölreserven basieren auf Selbstdeklarationen der OPEC-Mitgliedstaaten und entziehen sich einer unabhängigen Überprüfung.

In Venezuelas Fall wurde ein erheblicher Teil des Orinoco-Schweröls erst durch mehrfache politische und ökonomisch grosszügige Auslegungen des Reservebegriffs in diese Kategorie gehoben, sowohl unter Chavez als auch unter Maduro: Förderbar gilt seither auch Öl, das nur unter idealisierten Preisannahmen, mit massiver und intakter Infrastruktur, stabilen Institutionen und erheblichem Kapitaleinsatz wirtschaftlich Sinn ergäbe.

Die formale Grösse der venezolanischen Reserven ist damit weniger Ausdruck realer Energieverfügbarkeit als das Resultat eines theoretischen Rechenmodells mit optimistischen Prämissen. Wer aus dieser Zahl unmittelbare strategische oder ökonomische Relevanz ableitet, verwechselt buchhalterisches Potenzial mit tatsächlicher Macht über Ressourcen.

Förderpotenzial trifft Investitionsrealität

Die Prognosen der internationalen Energieagentur IEA deuten darauf hin, dass das weltweite Angebot die Nachfrage noch Jahre übersteigen wird, mit entsprechendem Druck auf die Preise.

Langfristig stellt sich deshalb eine grundlegendere Frage: Wie wertvoll ist Venezuelas Öl überhaupt? Zwar sind die Reserven beträchtlich, auch wenn sie unter den offiziellen Zahlen liegen mögen, doch klar ist, dass der überwiegende Teil aus dem Orinoco-Schweröl besteht, dessen Förderung besonders teuer und technisch anspruchsvoll ist. In einem globalen Energiemarkt, der zunehmend von Überangebot, Kostendruck und einem strukturellen Wandel der Nachfrage geprägt ist, wären venezolanische Ölfelder unter solchen Bedingungen laut Bloomberg-Stratege Julian Lee deshalb kaum profitabel.

Unstrittig ist, dass Venezuelas Ölindustrie seit der Chavez-Periode in einem desolaten Zustand ist. Misswirtschaft, politische Eingriffe und Unterinvestitionen haben die Förderung von über drei Millionen Barrel pro Tag auf rund eine Million reduziert. Selbst bei einem reibungslosen politischen Übergang und einer vollständigen Aufhebung der US-Sanktionen wäre gemäss Lee eine rasche Erholung unrealistisch.

Hinzu kommt der enorme Kapitalbedarf. Um die Förderung auch nur auf das Niveau der frühen 2010er-Jahre zurückzubringen, wären laut Experten Investitionen in die Infrastruktur von mehreren 100 Milliarden Dollar nötig. Soll Venezuela perspektivisch eine Exportkapazität erreichen, die mit kanadischem Schweröl vergleichbar ist, also rund drei Millionen Barrel pro Tag, belaufen sich die Gesamtkosten auf nahezu eine Billion US-Dollar.

Bereits heute fehlt es an grundlegender Infrastruktur: Raffinerien müssten technisch umgerüstet, Exportterminals erweitert, neue Pipelines gebaut und Stromkapazitäten massiv ausgebaut werden. Venezuela verfügt über keine laufenden SAGD-Projekte (Schwerölförderung) wie in Kanada. Jedes neue Projekt wäre ein sogenanntes Greenfield-Vorhaben mit entsprechend hohen Einstiegskosten. Diese liegen bei etwa 30 bis 45 US-Dollar pro gefördertem Barrel pro Tag, also knapp eine Milliarde Dollar für einen Zuwachs von lediglich 30.000 Barrel pro Tag und das innerhalb von rund drei Jahren.

Die aktuelle Förderung basiert grösstenteils auf dem vergleichsweise einfachen, aber ineffizienten «Cold Production»-Verfahren, bei dem das Öl durch abnehmenden Lagerstättendruck an die Oberfläche gelangt. Dieses Verfahren ist zwar kurzfristig günstiger, liefert jedoch deutlich niedrigere Förderraten. Zudem ist man dabei auf grosse Mengen an Verdünnungsmitteln und Polymeren angewiesen, sogenannte Enhanced Oil Recovery (EOR)-Technologien, die wiederum eigene Infrastruktur, chemische Lieferketten und hohe Betriebskosten erfordern. Auch die Stromversorgung ist ein zentrales Problem: Weite Teile Venezuelas leiden unter chronischen Blackouts, während der Aufbau einer zuverlässigen Energieversorgung für thermische Verfahren wie SAGD weitere Milliardeninvestitionen erfordert. Bei den aktuellen Ölpreisen lässt sich die für ein substanzielles Produktionswachstum nötige Kapitalmenge kaum rechtfertigen. Ob amerikanische Ölkonzerne tatsächlich bereit wären, dieses Risiko einzugehen, ist daher keineswegs so selbstverständlich, wie das Trump angekündigt hat.

Quelle: Bloomberg Financial LP

Auch institutionell ist die Ausgangslage problematisch. Der staatliche Ölkonzern PDVSA leidet, wie das ganze Land, unter massiver Abwanderung von Fachkräften und wird inzwischen weitgehend vom Militär kontrolliert. Ohne tiefgreifende Reformen wäre er auf Jahre hinaus kein verlässlicher Partner für westliche Unternehmen. Selbst wenn Kapital und Technik verfügbar wären, fehlt es an personellen und organisatorischen Voraussetzungen, um ein solch gigantisches Infrastrukturprojekt in einem heruntergewirtschafteten Land effizient umzusetzen.

Weitere Rohstoffe

Erdöl dominiert klar Venezuelas Rohstofflandschaft. Weitere Ressourcen sind zwar reichlich vorhanden, werden aber kaum exportiert. In Zusammenhang mit der Erdölproduktion steht Erdgas, welches zu einem grossen Teil bei der Ölförderung anfällt. Die Förderung und kommerzielle Nutzung sind im Vergleich zu den Reserven aber gering. Die Goldvorkommen von Venezuela sind beachtlich und gehören wahrscheinlich zu den 10 grössten der Erde. Die offiziellen Schätzungen unterliegen jedoch grossen Schwankungen und sind nicht gesichert. In Eisenerz und Bauxit, das für Herstellung von Aluminium verwendet wird, bestehen weitere «bedeutende» Vorkommen.

Fazit

Die Reaktion der Märkte

Venezolanische Staatsanleihen haben am Montag nach der Festnahme von Nicolás Maduros heftig zugelegt – teils über 20%. Der Regierungswechsel und eine stabilere und global akzeptierte Staatsführung werden vom Markt klar begrüsst. Amerikanische Treasuries notieren praktisch unverändert.

US-Energie- und Öl-Aktien legen nach der Intervention und der in Aussicht gestellten Investitionen amerikanischen Ölfirmen in die marode venezolanische Förder- und Raffinerieinfrastruktur deutlich zu. Der erwartete Zugang zu den erheblichen Ölreserven Venezuelas erlaubt eine nachhaltig positive Einschätzung.

Durch den Angriff der USA auf Venezuela droht die geopolitische Situation zu eskalieren, da sich andere Regierungen ermutigt sehen, vergleichbare Übergriffe durchzuführen. Als Folge dürften Edelmetalle ihren Lauf von 2025 fortsetzen, wenngleich mit abgeschwächter Dynamik.

Stärkung der US-Hegemonie

Die militärische Festsetzung von Nicolás Maduro ist eine Machtdemonstration. Sie sendet ein klares Signal an Gegner und Partner gleichermassen, dass die USA bereit und fähig sind, ihre Interessen auch jenseits diplomatischer Mittel durchzusetzen. Das Signal aus Caracas ist dabei unmissverständlich: Die Vereinigten Staaten werden die aktualisierte sicherheitspolitische Doktrin in ihrem geopolitischen «Vorgarten» nach unserer Einschätzung konsequent und bedingungslos umsetzen.

Die Operation kann zugleich als Teil eines umfassenderen strategischen Wettbewerbs mit China verstanden werden, insbesondere in Form einer faktischen «Gegenblockade» in der westlichen Hemisphäre. Durch die Entmachtung Maduros wurden chinesische Investitionen im venezolanischen Ölsektor abrupt entwertet; gleichzeitig verlor Russland ebenso wie Iran einen wichtigen politischen und operativen Brückenkopf in Lateinamerika. In diesem Sinne ist der Eingriff weniger als isolierte Intervention denn als strukturelle Verschiebung regionaler Machtverhältnisse zu interpretieren.

Für die USA kommt hinzu, dass ihre derzeit beträchtliche Abhängigkeit von kanadischem Schweröl strategische Verwundbarkeiten schafft, die Washington mittelfristig zu diversifizieren sucht. Venezuela bietet aus rein geologischer Sicht eine naheliegende Ergänzung. Ob es jedoch gelingt, die zerstörte Infrastruktur rasch zu erneuern, eine verlässliche Lieferkette in die USA aufzubauen und die umfangreichen Ölreserven tatsächlich profitabel zu monetarisieren, bleibt offen. Entscheidend ist weniger die kurzfristige Produktionsperspektive als die veränderte Kontrollstruktur: Die operative und strategische Hoheit liegt nun bei den USA – nicht mehr bei China.

Das strategische Momentum geht damit klar an Washington, was Peking und Moskau vorerst in die Defensive drängt. Beide reagierten zwar rhetorisch scharf, vermieden bislang jedoch konkrete Gegenmassnahmen. Das Schweigen vieler weiterer Regierungen wird teils als stillschweigende Akzeptanz, teils als Ausdruck diplomatischer Ohnmacht interpretiert.

Risiko langfristiger Instabilität

Dennoch lauern mögliche strategischen Folgekosten. Die Lage in Venezuela bleibt fragil; ob die USA eine nachhaltige politische Ordnung etablieren können, ist offen. Historische Vergleiche (Irak, Libyen) zeigen, dass Regimewechsel zwar militärisch durchführbar sind, aber die Phase danach meist komplex, teuer und innenpolitisch riskant wird. Einige Strategen sprechen bereits von einer möglichen «Sicherheitsfalle», in der die USA nun gezwungen sein könnten, das Land über Jahre hinweg zu stabilisieren, politisch, wirtschaftlich und ggf. auch militärisch.

Internationale Normverschiebung

Die US-Intervention könnte Signalwirkung für weitere Länder haben. Wenn für die Erreichung strategischer Interessen, wie Wiederherstellung historischer Grenzlinien oder den Zugang zu Rohstoffen, die Machtpolitik über das Völkerrecht gestellt wird, lassen sich auch Angriffe auf die Ukraine oder Taiwan rechtfertigen. Die Schwelle für «legitime Gewaltanwendung» im geopolitischen Kontext sinkt. Das Bedrohungspotenzial umfasst aber auch die Blockbildung antiwestlicher Allianzen, wie BRICS+ oder die Schwächung internationaler Institutionen wie die Uno oder Menschenrechtkonventionen. Die globale Ordnung, wie wir sie seit dem 2. Weltkrieg kennen, ist gefährdet.

Positionierung

Bestätigung statt Reaktion

Spätestens jetzt sollte klar sein, dass Trump 2.0 nicht nur symbolische Rhetorik betreibt, sondern die im Wahlkampf formulierten Ziele konsequent in konkrete Aktionen überführt, militärisch wie wirtschaftlich.

Unser Fokus bleibt daher gezielt auf jenen Politikfeldern, die mittel- und langfristig die Märkte dominieren werden, allen voran Trumps geld- und fiskalpolitische Agenda. Wie bereits in früheren Publikationen skizziert, gehen wir davon aus, dass nicht politische Gegenspieler, sondern einzig der Bondmarkt Trump Grenzen aufzeigen kann, indem er über steigende Renditen die Refinanzierungskosten für den Staat in potenziell schmerzhafte Höhen treibt.

Das weiss auch Trump und entsprechend intensiviert er den Druck auf die Fed, die Zinsen zu senken. Doch es geht nicht nur um den Leitzins: auch die langfristigen Zinsen müssen unter Kontrolle gehalten werden. Zentral in diesem Kalkül ist Trumps Bestreben, die unabhängige Fed unter politische Kontrolle zu bringen, etwa durch die Einsetzung eines loyalen Vorsitzenden, der als de-facto-Garantiegeber für den US-Staatsanleihemarkt fungiert. Sollte dieser Plan Realität werden, würde sich ein massiver Eingriff in die Marktmechanik der US-Renditen vollziehen, mit tiefgreifenden Folgen für Anleihemärkte, Währung und Inflation. Denn: Gibt es kein Ventil bei den Zinsen, verlagert sich der Druck auf die Währung.

Wie das Beispiel Japan zeigt, können stark unterdrückte Realzinsen bei gleichzeitiger expansiver Schuldenpolitik zu einem strukturell schwachen Wechselkurs führen.

Übertragen auf die USA bedeutet das: Sollte Trump seine Pläne mit Konsequenz verfolgen, dürfte der US-Dollar strukturell unter Druck geraten. In Kombination mit einer fortgesetzt expansiven Fiskalpolitik erhöht das die Wahrscheinlichkeit für eine anhaltend erhöhte Inflation in den kommenden Jahren, selbst wenn sich kurzfristig geopolitische Stabilität vorgaukeln lässt. Die spektakuläre US-Intervention in Venezuela markiert ohne Zweifel einen geopolitischen Wendepunkt. Doch leiten wir daraus keine unmittelbaren Anpassungen unserer taktischen Positionierung ab. Vielmehr sehen wir uns in unserer bisherigen Einschätzung bestätigt: Gold bleibt übergewichtet, als Schutz vor politischer Unsicherheit, Inflationsrisiken und zunehmender Staatsverschuldung. Alternative Anlagen wie Immobilien, CAT-Bonds oder CTAs bieten aus unserer Sicht die überzeugenderen Diversifikations-Profile im Vergleich zu traditionellen Anleihen, die wir weiterhin klar untergewichten und konsequent in Schweizer Franken absichern.

Aquila Investment Management

CIO Office

Silvano Marchesi

Chief Investment Officer

Tel. +41 58 680 60 40

Disclaimer: Produced by Investment Center Aquila Ltd.

Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no under-taking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information pro-vided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other trans

action. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.