This website uses cookies. For more information about this and your rights as a user, please see our Privacy policy.

To use our website, you must accept our privacy policy.

The US intervention in Venezuela marks a geopolitical turning point and the first concrete implementation of the updated US doctrine in the Western hemisphere. The overthrow of Maduro is less an isolated military action than a strategic demonstration of power vis-à-vis China, Russia and Iran. Chinese investments in the oil sector have been effectively devalued and control over Venezuela's resources now lies with the USA.

Despite considerable reserves, high investment costs, institutional weaknesses and fragile stability remain key risks. We are not making any immediate tactical adjustments, but see our strategic orientation confirmed. Gold remains overweight as insurance against geopolitical escalation, inflation risks and fiscal indiscipline, while we continue to underweight traditional bonds and consistently hedge in CHF.

The event

What happened?

In the early hours of January 3, 2026, US forces launched targeted attacks on the Venezuelan capital Caracas in a wide-ranging military operation. Numerous explosions rocked the city, including attacks on military installations such as the La Carlota air base and anti-aircraft defense systems. The declared main objective: the arrest of President Nicolás Maduro.

Special forces, who were already involved in the killing of Osama bin Laden, broke into the presidential palace, arrested Maduro and his wife Cilia Flores and flew them both to a US warship in the Caribbean. From there they were transferred to New York, where they are being held in the Metropolitan Detention Center.

According to official information, the operation lasted less than three hours and met with no significant resistance from the Venezuelan armed forces. It took place against the backdrop of months of political tensions between Washington and Caracas, which had recently intensified significantly. According to the US government, the operation was also based on "concrete security findings" that made immediate intervention necessary.

The Venezuelan government described the action as an "illegal invasion" and spoke of a serious breach of international law.

On 4 January, the US Department of Justice immediately brought charges against Maduro and five other individuals for their alleged roles in a drug trafficking network and for collaborating with groups that the US classifies as foreign terrorist organizations. Maduro has vehemently denied these accusations before and now also in the indictment.

Voices from official sites

Following the military operation in Venezuela, representatives of the US government and international players used some drastic words. US President Donald Trump repeatedly described the operation as an extraordinary success. At a press conference, he said: "This was one of the most impressive, effective and powerful military actions by the United States." Trump described the operation as an "attack the likes of which have not been seen since World War II" and announced: "We will remain in the country until a safe, orderly and responsible transition is possible."

Trump also announced economic ambitions in Venezuela: "Our very large US oil companies, the largest in the world, will invest there, spend billions, repair the broken infrastructure and start making money for the country."

Defense Minister Pete Hegseth explained that the operation was the result of months of planning. He said of Maduro: "He had his chance, just as Iran had its chance. But then it was over. He overdid it and suffered the consequences."

General Dan Caine, Chairman of the Joint Chiefs of Staff, explained the operation, codenamed "Operation Absolute Resolve": "The operation was discreet, precise and carried out in the darkest hours of January 2nd. It was the result of months of planning and preparation. An operation that only the US military can carry out."

The declared war on drug trafficking

A central motive of the US government for its intervention is the accusation that Venezuela, along with other South American states, is an active part of the international drug trade under Nicolás Maduro.

The Venezuelan opposition leader María Corina Machado painted a similarly gloomy picture. At a press conference in Norway 2025, she said: "Some people are talking about an invasion of Venezuela. My answer is that this has already happened. Russian agents, Iranian agents, terrorist groups such as Hezbollah and Hamas operate freely according to the regime's instructions. Colombian guerrillas and drug cartels control sixty percent of our population. It's not just about drugs, but also about human trafficking and prostitution. Venezuela has become the criminal center of the Americas."

These statements underscore the narrative that Venezuela is no longer perceived merely as an authoritarian regime, but as a transnational criminal network with a direct impact on US security.

Trump explicitly positioned the operation in Venezuela as part of a broader security policy strategy. He also referred to historical US doctrines: "The Monroe Doctrine was important, but we've gone much further. Some now call it the 'Donroe Doctrine', but I don't know exactly."

The statements show that the US government under Trump is not just looking at Venezuela. He went on to say in a press conference: "[Colombian President] Petro is producing cocaine that is coming into the United States, so he better watch himself." When asked by a reporter whether an operation against Colombia was imminent, Trump replied: "Sounds good to me." Mexico was also sharply criticized: "Something has to be done with Mexico, too. It's not ruled by a president, it's ruled by cartels."

Foreign Minister Marco Rubio also emphasized the strategic importance of the action: "This is the Western Hemisphere. We will not allow our adversaries to establish a base of operations here ... This is over." With regard to Cuba, he added: "If I were part of the Cuban leadership, I would be very worried right now."

Maduro's arrest is therefore seen as a signal in Washington: The fight against organized crime is being waged militarily and Latin America is under observation. A return to the previous restraint does not appear to be planned.

The "Donroe Doctrine": a new era of American dominance in the Western Hemisphere?

In the United States National Security Strategy of November 2025, the US government announced a fundamental realignment of its foreign and security policy in the Western Hemisphere. Building on the historic Monroe Doctrine, the document formulates a modernized guideline known as the "Trump Corollary to the Monroe Doctrine" and, as mentioned, is also referred to by critics and supporters as the "Donroe Doctrine".

The aim is to restore and secure the supremacy of the USA in the western hemisphere. It reads: "After years of neglect, America will reassert and enforce the Monroe Doctrine to restore American supremacy in the Western Hemisphere."

Among other things, the strategy envisages denying non-hemispheric competitors - primarily China, Russia and Iran - access to critical resources, military presence or infrastructure in the American sphere of influence. According to the strategy, the US claims the right to prevent foreign influence by any means necessary: "We want other states to view us as a preferred partner and we will (in various ways) discourage their cooperation with others."

It also calls on Latin American governments to cooperate more closely with the US, particularly in the fight against drug cartels, transnational crime and migration. It also states that the hemisphere should be free from "hostile foreign influence or ownership of strategic assets", instead supporting critical supply chains and securing US access to key regions.

The "Donroe Doctrine" therefore represents a geopolitical clarification: The USA claims the western hemisphere as its own security policy area and is prepared to secure this position militarily and economically. The operation in Venezuela can therefore be interpreted as the first concrete implementation of this new strategic line.

However, this is not just about domestic political stabilization or the fight against organized crime. At its heart is also a geopolitical trial of strength with China. After all, the operation in Venezuela not only removed an authoritarian regime from power, but also cut one of Beijing's most important energy connections in the western hemisphere.

China's investments in Venezuela

China has invested heavily in Venezuela over the past two decades, primarily through oil-backed loans. Between 2007 and 2015, Beijing provided the country with more than 60 billion US dollars in financing: Money that Caracas was supposed to pay back to China with long-term oil supply contracts. This sum was equivalent to around 16% of Venezuelan GDP and made China Venezuela's largest lender.

Without the Chinese loans, Venezuela would probably have run into payment difficulties years ago. Tens of billions are still outstanding today; estimates put the outstanding loans linked to oil at around 19 billion US dollars.

In addition to the loans, Chinese companies, mostly state-owned oil companies, had negotiated stakes in Venezuelan oil fields and long-term production agreements. It was not until 2024 that a private Chinese company, China Concord Resources Corp. (CCRC), signed a 20-year production contract to expand oil production in Venezuela.

After the forced change of power in Caracas, however, all of these deals are in danger of becoming invalid. The previously "ironclad" contractual rights of Chinese players could effectively be worthless.

The direct oil supply relationship between Venezuela and China is also on the verge of collapse. As a result of US sanctions since 2019, China has replaced the Western market as the main buyer of Venezuelan oil. Most recently, it was estimated that up to 80% of Venezuelan oil exports went to China. This corresponded to around 750,000 barrels of crude oil per day, which were purchased by Chinese importers, allowing the Maduro regime to earn a minimal amount of foreign currency. By comparison, this volume accounted for around 4% of total Chinese crude oil imports.

For China, Venezuelan oil was therefore only a small part of the import portfolio in terms of volume, but nevertheless strategically important. On the one hand, it was heavy crude oil from the Orinoco Belt, which a number of Chinese refineries are designed to process. Secondly, Venezuela's crude oil was traded at high discounts due to the sanctions, with estimates of 30% or more below market. Access to this heavily discounted heavy oil was crucial for Chinese refineries in order to secure their already tight margins.

Independent Chinese refineries in particular, known as "teapots", readily seized the opportunity, despite the sanctions risks: according to Reuters, around two thirds of China's Venezuelan oil imports ended up with these smaller refineries, which were able to process the crude oil more profitably thanks to the discounts. The remaining third of deliveries went directly to Chinese creditors as repayment for the high loans to Caracas. If the US sanctions were lifted or the oil diverted elsewhere, China would lose out twice over, as the refiners would have to switch to more expensive heavy crude oil from other sources and the repayment of the loans through oil would be in question.

In fact, the consequences of the US intervention are already becoming apparent. Immediately after the strike on Caracas, several oil tankers changed their route. According to the Wall Street Journal, the Chinese supertanker "Thousand Sunny", which was on its way to Venezuela, turned around and set course for Nigeria. Other tankers dropped anchor.

Beijing's rhetoric was correspondingly harsh: it was "deeply shocked" and condemned the "reckless use of force" by the US, the Chinese Foreign Ministry declared a few hours after the night-time explosions in Caracas. Washington's actions constituted a "serious violation of international law" and Venezuela's sovereignty, according to the accusation from Beijing.

A precedent for Taiwan?

Most current analyses contain no indication that China sees the US military action in Venezuela as carte blanche for its own violent "solution" to the Taiwan issue.

Beijing is using the incident to brand the US as a hegemonic lawbreaker. The idea of a "precedent" is also the subject of lively discussion in the Chinese online public, in some cases triumphantly as a "prime example" of an attack against Taiwan.

However, officials in Beijing clearly separate the Taiwan issue from the Venezuela event and renowned Chinese experts emphasize that an attack on Taiwan would be determined by China's own capabilities and interests, not by US interventions elsewhere.

Western security experts support this view: despite some fears of a new escalation logic, the majority opinion is that Xi Jinping's calculation remains unchanged and that he does not need (or seek) an additional reason to take action against Taiwan one day if circumstances require it from the Chinese perspective.

Nevertheless, the US deployment has crossed a symbolic threshold that is being felt globally. It provides China with "cheap ammunition" in the diplomatic dispute and could serve as a long-term argument to justify its own robust actions. For Taiwan, the episode means increased vigilance: the island republic will want to further strengthen its defense and tie itself even more closely to the USA.

But how high is the actual risk of a Chinese invasion of Taiwan? Let's follow the money: a look at the markets that allow betting on political events, such as polymarket.com, suggests that the perceived probability of a short-term escalation is rather low. For example, the implied probability of an invasion by the end of March 2026 is only 4%, rising moderately to 7% by the end of June 2026 and reaching around 13% for the tenor by the end of 2026.

Source: polymarket

So far, the attack on Venezuela has not triggered an immediate threat of war in East Asia, but the erosion of previous taboos in international politics is unmistakable and is causing tense calculations for the future on all sides.

Motivation

Is it the oil?

Back to "black gold": is the USA targeting Venezuela's reserves? At first glance, this assumption seems surprising. Since the so-called shale oil revolution, the USA has been producing more oil than ever before, significantly exceeding the production of many traditional oil-producing countries. Venezuela, on the other hand, has become one of the smaller producers under decades of socialist leadership and the associated American sanctions in recent years. So why should Washington be interested in Venezuelan oil of all things?

According to Sky analyst Ed Conway, the answer lies not in the quantity, but in the type of oil. Not all crude oil is the same. Depending on the geological conditions, a distinction is made between light, medium and heavy crude oil. Light oil is thin and relatively easy to process, whereas heavy oil is viscous, tar-like and technically more demanding. It often has to be diluted before it can be transported through pipelines.

This is precisely the crucial point: the American shale oil extracted by fracking is predominantly light crude oil.

Before the breakthrough of fracking technology, American oil production was concentrated on conventional fields, for example in Texas, California and Alaska, whose crude oil qualities tended to be heavy or medium. The largest US refineries, particularly on the Gulf Coast in Texas and Louisiana, were therefore designed for decades to process heavy crude oil. These plants cannot be converted without enormous financial outlay, if it is possible at all. In order to produce gasoline, diesel and other products in sufficient quantities, they still need heavy crude oil grades to utilize their capacity.

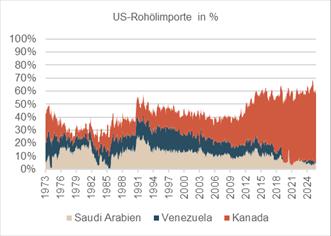

Although the USA is now producing more oil than ever before, it is still heavily reliant on imports, especially heavy crude oil. While only a small proportion of imports used to consist of this particularly dense form of oil, heavy grades now make up the majority of US oil imports.

The most important suppliers of this heavy crude oil are Russia, Canada, Mexico and potentially Venezuela. In fact, the majority of US imports today come from Canada, while Venezuela hardly plays a role anymore due to political tensions and sanctions.

Source: U.S. Energy Information Administration

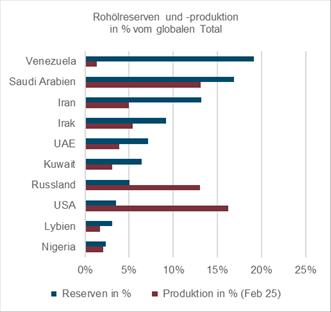

But it is precisely here that the strategic dimension becomes apparent. A look at the global oil reserves shows why Venezuela could be important for the USA in the long term. The country has the largest proven oil reserves in the world, ahead of countries such as Saudi Arabia, Iran and Iraq. Most of this is precisely the heavy oil that American refineries need.

Source: OPEC

The thing with the numbers

The underlying figures on oil reserves are based on self-declarations by OPEC member states and are not subject to independent verification.

In Venezuela's case, a significant portion of the Orinoco heavy oil was only elevated to this category through multiple politically and economically generous interpretations of the reserve concept, both under Chavez and Maduro: since then, oil that would only make economic sense under idealized price assumptions, with massive and intact infrastructure, stable institutions and considerable capital investment has also been considered recoverable.

The formal size of the Venezuelan reserves is therefore less an expression of real energy availability than the result of a theoretical calculation model with optimistic premises. Anyone who derives direct strategic or economic relevance from this figure is confusing accounting potential with actual power over resources.

Funding potential meets investment reality

Forecasts by the International Energy Agency (IEA) indicate that global supply will continue to exceed demand for years to come, with corresponding pressure on prices.

In the long term, this raises a more fundamental question: how valuable is Venezuela's oil anyway? Although the reserves are considerable, even if they may be lower than the official figures, it is clear that the majority consists of Orinoco heavy oil, which is particularly expensive and technically challenging to extract. In a global energy market that is increasingly characterized by oversupply, cost pressure and a structural change in demand, Venezuelan oil fields would therefore hardly be profitable under such conditions, according to Bloomberg strategist Julian Lee.

It is undisputed that Venezuela's oil industry has been in a desolate state since the Chavez period. Mismanagement, political intervention and underinvestment have reduced production from over three million barrels per day to around one million. Even with a smooth political transition and a complete lifting of US sanctions, a rapid recovery would be unrealistic, according to Lee.

Added to this is the enormous capital requirement. According to experts, investments in infrastructure of several hundred billion dollars would be required to even bring production back to the level of the early 2010s. If Venezuela is to achieve an export capacity comparable to Canadian heavy oil in the future, i.e. around three million barrels per day, the total costs would amount to almost one trillion US dollars.

There is already a lack of basic infrastructure: refineries would have to be technically upgraded, export terminals expanded, new pipelines built and electricity capacities massively expanded. Venezuela has no ongoing SAGD projects (heavy oil production) like in Canada. Any new project would be a so-called greenfield project with correspondingly high entry costs. These are around 30 to 45 US dollars per barrel produced per day, i.e. almost one billion dollars for an increase of just 30,000 barrels per day within around three years.

Current production is largely based on the comparatively simple but inefficient "cold production" process, in which the oil is brought to the surface by decreasing reservoir pressure. Although this process is cheaper in the short term, it delivers significantly lower production rates. It also relies on large quantities of diluents and polymers, known as enhanced oil recovery (EOR) technologies, which in turn require their own infrastructure, chemical supply chains and high operating costs. The power supply is also a key problem: large parts of Venezuela suffer from chronic blackouts, while the establishment of a reliable energy supply for thermal processes such as SAGD requires billions in further investment. At current oil prices, the amount of capital required for substantial production growth can hardly be justified. Whether American oil companies would actually be prepared to take this risk is therefore by no means as self-evident as Trump has announced.

Source: Bloomberg Financial LP

The initial situation is also problematic in institutional terms. The state oil company PDVSA, like the entire country, is suffering from a massive brain drain and is now largely controlled by the military. Without far-reaching reforms, it would not be a reliable partner for Western companies for years to come. Even if capital and technology were available, there is a lack of human and organizational resources to efficiently implement such a gigantic infrastructure project in a run-down country.

Other raw materials

Oil clearly dominates Venezuela's raw materials landscape. Although other resources are abundant, they are hardly exported. Natural gas is linked to oil production and is largely produced during oil extraction. However, production and commercial use are low compared to the reserves. Venezuela's gold deposits are considerable and are probably among the 10 largest in the world. However, the official estimates are subject to major fluctuations and are not certain. Other "significant" deposits exist in iron ore and bauxite, which is used for the production of aluminum.

Conclusion

The reaction of the markets

Venezuelan government bonds rose sharply on Monday following the arrest of Nicolás Maduro - in some cases by over 20%. The change of government and a more stable and globally accepted leadership are clearly welcomed by the market. American Treasuries are virtually unchanged.

US energy and oil shares have risen significantly following the intervention and the prospect of American oil companies investing in the ailing Venezuelan production and refinery infrastructure. The expected access to Venezuela's considerable oil reserves allows for a sustained positive assessment.

The US attack on Venezuela threatens to escalate the geopolitical situation, as other governments feel emboldened to carry out similar attacks. As a result, precious metals are likely to continue their 2025 run, albeit at a slower pace.

Strengthening US hegemony

The military arrest of Nicolás Maduro is a demonstration of power. It sends a clear signal to opponents and partners alike that the US is willing and able to assert its interests beyond diplomatic means. The signal from Caracas is unmistakable: in our view, the United States will consistently and unconditionally implement the updated security policy doctrine in its geopolitical "front yard".

The operation can also be seen as part of a broader strategic competition with China, particularly in the form of a de facto "counter-blockade" in the western hemisphere. Maduro's removal from power abruptly devalued Chinese investments in the Venezuelan oil sector; at the same time, Russia, like Iran, lost an important political and operational bridgehead in Latin America. In this sense, the intervention should be interpreted less as an isolated intervention than as a structural shift in regional power relations.

For the USA, there is also the fact that its current considerable dependence on Canadian heavy oil creates strategic vulnerabilities that Washington is seeking to diversify in the medium term. Venezuela is an obvious addition from a purely geological perspective. However, it remains to be seen whether it will be possible to quickly renew the destroyed infrastructure, establish a reliable supply chain to the USA and actually monetize the extensive oil reserves profitably. The decisive factor is less the short-term production perspective than the changed control structure: operational and strategic sovereignty now lies with the USA - no longer with China.

The strategic momentum is thus clearly in Washington's favor, which is putting Beijing and Moscow on the defensive for the time being. Although both have reacted sharply in rhetorical terms, they have so far avoided concrete countermeasures. The silence of many other governments is being interpreted partly as tacit acceptance and partly as an expression of diplomatic impotence.

Risk of long-term instability

Nevertheless, potential strategic follow-up costs lurk. The situation in Venezuela remains fragile; whether the USA can establish a sustainable political order remains to be seen. Historical comparisons (Iraq, Libya) show that although regime change is militarily feasible, the subsequent phase is usually complex, expensive and domestically risky. Some strategists are already talking about a possible "security trap" in which the USA could now be forced to stabilize the country for years, politically, economically and possibly also militarily.

International shift in standards

The US intervention could send a signal to other countries. If power politics is placed above international law in order to achieve strategic interests, such as the restoration of historical borderlines or access to raw materials, attacks on Ukraine or Taiwan can also be justified. The threshold for the "legitimate use of force" in a geopolitical context is falling. However, the potential threat also includes the formation of blocs of anti-Western alliances such as BRICS+ or the weakening of international institutions such as the UN or human rights conventions. The global order as we have known it since the Second World War is under threat.

Positioning

Confirmation instead of reaction

By now at the latest, it should be clear that Trump 2.0 is not just engaging in symbolic rhetoric, but is consistently translating the goals formulated in the election campaign into concrete actions, both militarily and economically.

Our focus therefore remains specifically on those policy areas that will dominate the markets in the medium and long term, above all Trump's monetary and fiscal policy agenda. As already outlined in previous publications, we assume that it is not political opponents but only the bond market that can show Trump the limits by driving up refinancing costs for the state to potentially painful heights through rising yields.

Trump knows this too and is therefore intensifying the pressure on the Fed to lower interest rates. But it is not just about the key interest rate: long-term interest rates must also be kept under control. Central to this calculation is Trump's desire to bring the independent Fed under political control, for example by appointing a loyal chairman who would act as a de facto guarantor for the US government bond market. If this plan were to become reality, there would be a massive intervention in the market mechanics of US yields, with far-reaching consequences for bond markets, the currency and inflation. After all, if there is no valve for interest rates, the pressure will shift to the currency.

As the example of Japan shows, strongly suppressed real interest rates combined with an expansionary debt policy can lead to a structurally weak exchange rate.

Applied to the US, this means that if Trump pursues his plans with consistency, the US dollar is likely to come under structural pressure. In combination with a continued expansionary fiscal policy, this increases the likelihood of persistently higher inflation in the coming years, even if geopolitical stability can be feigned in the short term. The spectacular US intervention in Venezuela undoubtedly marks a geopolitical turning point. However, we are not making any immediate adjustments to our tactical positioning as a result. Rather, we see our previous assessment confirmed: Gold remains overweight as protection against political uncertainty, inflation risks and increasing government debt. In our view, alternative investments such as real estate, CAT bonds or CTAs offer the more convincing diversification profiles compared to traditional bonds, which we continue to clearly underweight and consistently hedge in Swiss francs.

Aquila Investment Management

CIO Office

Silvano Marchesi

Chief Investment Officer

Phone +41 58 680 60 40

Disclaimer: Produced by Investment Center Aquila Ltd.

Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no under-taking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information pro-vided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other trans

action. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.