This website uses cookies. For more information about this and your rights as a user, please see our Privacy policy.

To use our website, you must accept our privacy policy.

Last Saturday, the USA and Israel attacked civilian and military targets in Iran. Ayatollah Ali Kamenei, the Iranian revolutionary leader, was killed in the attack. The Iranian government has announced 40 days of national mourning.

Iran has responded with counter-attacks on Israel and on American military bases in several Arab Gulf states. There is a risk of the armed conflict spreading to neighboring states and the fighting lasting longer. This raises questions about the issue of ammunition and supplies on the side of both warring parties. After the 12-day war in 2025, Iran's stocks have been greatly reduced and supplies from China and Russia are unclear. Although the USA has moved parts of its navy to the region and pooled resources in Europe, the short preparation time raises questions about its operational capability. Due to its support for Ukraine in the war against Russia, the USA could also face supply bottlenecks for some weapons systems.

International reactions to the escalation in the region were mixed. Russia made cynical comments about «peacemaker Trump» and condemned the attack on Iran in the strongest possible terms. In Europe, Macron, Merz and Starmer joined forces to issue a joint statement against Iran's attacks on Israel and neighboring countries and called on the parties to resume diplomatic talks. These were abruptly broken off at the end of last week in Geneva without success.

Geopolitical risks have risen massively in connection with the escalation in the region. This is likely to have an impact on the commodities sector in particular.

Precious metals are the first beneficiaries here and, secondly, price rises in energy commodities are to be expected. The latter depend on Iran's measures in the Strait of Hormuz. Over 20% of the world's energy commodities are transported via this route. A blockade could cause prices to skyrocket, massively restrict the supply situation and fuel global inflation, which is likely to displease Donald Trump, as his poll ratings are already at historic lows of all previous presidents in this century due to the high cost of living.

Strategic classification - what does each side want?

In order to classify the situation correctly, it is worth taking a sober look at the strategic interests of the players involved.

The United States

From Washington's perspective, Iran has been a key security policy problem in the Middle East for years. Tehran provides military and financial support to a number of non-state actors, including Hezbollah, Hamas and Shiite militias in Iraq. These groups contribute significantly to instability in several states. Iran also has an advanced missile program and, according to Western assessments, continues to pursue nuclear ambitions. At the same time, a large proportion of global energy trade takes place through the strategically important «Strait of Hormuz», which is of considerable importance to the global economy.

Against this backdrop, the United States is not only concerned with reducing Iran's military capabilities, but also with maintaining a broader strategic influence in a potentially unstable region. A military strike is aimed at weakening key defense capabilities - such as missile sites or infrastructure that could potentially contribute to the production or proliferation of ballistic systems.

Furthermore, the US leadership is openly pursuing the goal of fundamentally changing the political course in Tehran. President Trump has repeatedly emphasized that the attacks are not solely for defensive purposes, but are aimed at permanently weakening the power structure in Iran and opening the way for internal political change. In public statements, he has directly addressed Iranian citizens and called for the removal of the current leadership.

Such steps have a dual strategic function. On the one hand, they send a clear signal of deterrence to potential geopolitical competitors: the USA is prepared to actively defend its interests. In international politics, the perception of determination counts, because threats lose weight if they are not backed up with action.

On the other hand, the domestic political dimension plays an important role. In times of geopolitical tensions, questions of national security become more important. History has shown that external conflicts can often lead to domestic political unity, at least temporarily. A clear, strategic step outwards can therefore create domestic political stability, even if the external cause remains controversial.

Israel

As mentioned, Iran supports several actors that directly challenge Israel's security. For Israel, however, this support is not just part of a regional power projection, but a concrete military threat with immediate reach.

From Israel's perspective, the combination of Iranian funding, technological support and strategic coordination of regional proxies is leading to a gradual military encirclement. The decisive factor here is not so much the individual organization as the overarching system behind it. Israel does not view Iran in isolation, but as the center of a network aimed at long-term strategic displacement.

The nuclear issue is particularly sensitive. Even if an Iranian program remains formally civilian, the ability to use it quickly for military purposes would fundamentally change the regional balance of power. For a small, territorially confined country with a high population density, strategic vulnerability has a different dimension than for major powers. Israel therefore calculates security risks with a much lower margin of error.

Against this backdrop, Israeli security doctrine has been based on a clear principle for decades: prevention is safer than reaction. This logic is not a short-term political reflex, but a deeply rooted part of the country's strategic culture. The current escalation is in line with this way of thinking. From an Israeli perspective, it is not about symbolic strength, but about the long-term prevention of a power imbalance that is perceived as existentially risky.

Iran

Iran's main priority in the current situation is its own survival. In military terms, Tehran is clearly inferior to the United States in a direct confrontation. A classic exchange of blows would therefore be neither realistic nor strategically sensible.

The Iranian strategy is traditionally asymmetrical. This means: no open field battle against the US army, but indirect countermeasures that are difficult to calculate. These include missile and drone attacks, the activation of allied militias in the region, cyber operations or targeted disruption of sensitive trade routes. Such measures are comparatively inexpensive, but significantly increase uncertainty and the burden on the other side.

The strategic calculation behind this is clear: to increase the costs for the opponent, economically, militarily and politically, without becoming embroiled in a full-scale war themselves. It is less about achieving a military victory and more about forcing the other side into a permanent, resource-intensive conflict.

As for the USA, the domestic political dimension plays a central role - albeit a mirror image. External threats often lead to temporary internal unity. This mechanism works not only in Western democracies, but also in authoritarian systems. An attack from outside shifts the political debate from the inside to the outside. Critical voices lose weight in the short term, and national identity and the will to resist come to the fore.

For the leadership in Tehran, external confrontation can therefore paradoxically have a stabilizing effect. Even if there are economic difficulties or social tensions, the focus is directed towards defending national sovereignty. In this sense, the domestic political effect of a conflict is an integral part of the strategic calculation for Iran - as it is for the USA.

Saudi Arabia

For Saudi Arabia, the conflict with Iran is less a security policy problem than a fundamental systemic rivalry. For decades, the two states have been competing for political, religious and strategic influence in the Middle East. Like Israel, Riyadh sees Tehran as a structural opponent for regional leadership claims. The conflict runs not only along geopolitical lines, but also along religious tensions between Sunni and Shiite forms of Islam. This dimension reinforces the ideological depth of the conflict and makes sustainable détente more difficult.

From the Saudi perspective, the threat manifests itself mainly indirectly: through Iranian influence in Yemen, Iraq, Syria and Lebanon. The vulnerability of the Saudi energy infrastructure is particularly sensitive. Attacks on oil facilities in recent years have shown how closely economic stability and national security are linked.

Against this backdrop, Saudi Arabia is pursuing a clear goal: the long-term containment of Iranian influence. A weakened Iran would significantly strengthen Riyadh's strategic position in the Gulf. At the same time, Saudi Arabia does not have the military means to conduct such a confrontation on its own. The country's security policy architecture is strongly oriented towards the United States.

This results in a double logic: on the one hand, Saudi Arabia benefits from a weakening of Iran. On the other hand, its own direct confrontation should remain as limited as possible. The optimal situation from the Saudi perspective is therefore a constellation in which external partners - in particular the USA - intervene decisively, while Riyadh provides strategic protection without becoming the main player in the conflict itself.

Everyone benefits?

Paradoxically, all governments involved can benefit from the escalation in the short term, albeit for different reasons.

For the USA and Israel, a decisive military response strengthens their deterrent effect and signals their ability to act vis-à-vis allies and rivals. For Saudi Arabia and Israel, weakening Iran means strategic relief in the regional power structure. And even for the leadership in Tehran, an external attack can have a stabilizing effect on domestic politics, as it creates national unity and overrides internal tensions. The same applies to the US government, which is struggling domestically.

Precisely because each side sees at least short-term advantages, whether strategic or domestic, the immediate incentive to de-escalate quickly is reduced.

Military overconfidence as a risk factor

The key question is therefore not whether an escalation can be explained politically, but whether it can be controlled militarily in the long term. This is where the real risk begins.

American military doctrine has changed since the early 2000s. Traditional principles, such as the mobilization of large ground forces, secure supply lines and the avoidance of encirclement, took a back seat. Instead, the concept of technological and intelligence superiority dominated: espionage, surveillance, air control, precision strikes, special forces.

This approach has enabled short-term successes. At the same time, it harbors a structural risk: the belief that conflicts everywhere can be resolved quickly and with limited means. However, the experience of recent decades, particularly in Vietnam and Afghanistan, shows that technological superiority alone does not necessarily neutralize asymmetric opponents. Military power is not synonymous with strategic control.

The structural logic of a soil invasion

Should the conflict develop beyond air and missile strikes into a more comprehensive military operation, the situation would become much more strategically challenging. Iran is not only geographically vast, but also topographically complex. Large parts of the country are characterized by mountain ranges, which complicates the movement of mechanized units and slows down military operations. Such terrain also increases the risk of deployed troops becoming isolated or effectively encircled, especially if supply routes are interrupted or attacked.

There is also the demographic dimension. With around 90 million inhabitants, Iran is one of the most populous countries in the region. Sustained control of larger areas would therefore require considerable human resources. Even a limited ground operation would have to be permanently secured, logistically supplied and politically legitimized.

Securing supply lines, maintaining a continuous troop presence and financing a prolonged engagement would tie up considerable economic and military resources. Historical experience shows that interventions in geographically complex and socially highly mobilizable states rarely last the originally calculated duration or cost structure.

The main risk therefore lies less in the initial phase of a military operation than in the phase afterwards - when a conflict is prolonged, a withdrawal becomes increasingly difficult politically and additional resources have to be deployed.

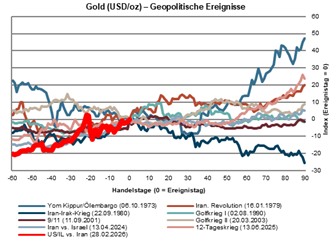

How did the markets react in the past?

A look at previous geopolitical escalations shows that the immediate market reaction is often characterized by increased volatility. A look at the three-month performance of gold following comparable geopolitical events shows a fundamentally constructive picture. The Iran-Iraq war in 1980 is a notable exception. Here, gold recorded a significant correction three months after the attack. However, the context is crucial: gold had previously appreciated massively in the wake of the Iranian revolution and high inflation in the USA and was in a speculative, over-extended phase at the beginning of 1980. The subsequent weakness was not so much an expression of a lack of crisis resistance, but rather a normalization after an exceptionally strong exaggeration.

Source: S&P Global

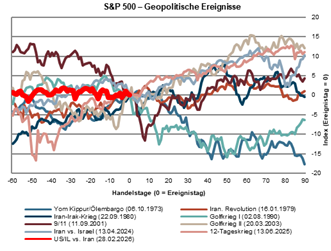

The S&P 500 also proved to be robust for the most part in such phases. After initial uncertainty, the markets often stabilized more quickly than expected - a pattern that corresponds to the well-known stock market saying «buy when the guns are blazing». The clearly negative three-month phases, such as 1973 or 1990, coincided with recessions in the USA. The decisive factor is therefore not so much the event itself, but the economic context. In a stable macroeconomic environment, stock markets tend to absorb geopolitical shocks within a few months.

Source: S&P Global

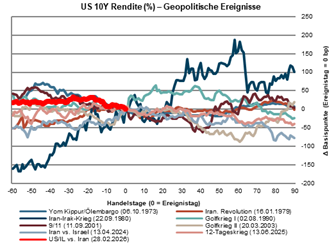

The development of yields on ten-year US government bonds shows no consistent pattern over three months.

Source: S&P Global

In some episodes, yields initially fell as a result of higher risk aversion, but rose again in the following months. In other cases, there was a direct increase, particularly when inflation or supply risks dominated.

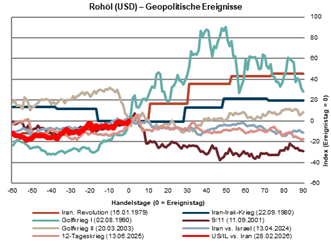

A differentiated picture emerged for oil over a three-month horizon.

Source: S&P Global

Significant and sustained price rises have historically occurred primarily in phases in which the oil price was still strongly determined by state or cartel-like pricing by the producing countries, particularly in the 1970s. In these regulated market structures, geopolitical shocks led directly to supply shocks and sustained price spikes.

Since oil has been traded on free futures markets, prices react sensitively to escalations in the short term, but tend to normalize in the medium term, provided there is no actual physical disruption to supply. The decisive factor is therefore less the military escalation itself than the question of whether there will be real production or transportation losses.

Positioning

From today's perspective, a short-term de-escalation seems unlikely. As outlined above, several governments are benefiting from the escalation dynamic, at least temporarily. At the same time, there is a risk of gradual overextension for the United States. Historical examples show that it is not the first military strike that is problematic, but the long-term commitment of resources in a potentially protracted and cost-intensive conflict.

Für die Kapitalmärkte bedeutet dies ein Umfeld erhöhter Volatilität in der kurzen Frist, jedoch nicht zwingend eine strukturelle Trendwende. An unserer taktischen Positionierung nehmen wir derzeit keine Änderungen vor. Zwar können Staatsanleihen kurzfristig von einer erhöhten Risikoaversion profitieren. Mittel- und langfristig bleiben sie jedoch aufgrund der hohen globalen Staatsverschuldung und der fehlenden fiskalischen Disziplin strukturell wenig attraktiv. Ein kostspieliger, langanhaltender militärischer Konflikt verbessert diese Ausgangslage nicht.

Wir bleiben in Gold übergewichtet und bevorzugen generell reale Vermögenswerte. Das Edelmetall dient als Absicherung gegen geopolitische Risiken, fiskalische Expansion und potenziell steigende Inflationsrisiken. Auch der Schweizer Franken dürfte als sicherer Hafen gesucht bleiben. An unserer neutralen Aktienallokation halten wir ebenfalls fest. Der Anlagefokus bleibt dabei klar auf Schweizer Dividenden- und Substanzaktien, die durch stabile Cashflows, solide Bilanzen und eine defensive Ertragsstruktur überzeugen.

Besondere Aufmerksamkeit gilt dem Energiemarkt. Rund 20 Prozent des weltweit gehandelten Öls passieren die Strasse von Hormus, eine Route, die vom Iran massgeblich beeinflusst oder im Extremfall blockiert werden kann. Eine nachhaltige Störung würde zu höheren Rohölpreisen führen, mit entsprechenden Auswirkungen auf globale Energiepreise. Dies könnte Inflations- und Rezessionsängste erneut verstärken – ein Szenario, das unsere Präferenz für Gold und realwertorientierte Anlagen zusätzlich untermauert.

Disclaimer: Produced by Investment Center Aquila Ltd.

Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no under-taking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information pro-vided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other trans

action. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.