This website uses cookies. For more information about this and your rights as a user, please see our Privacy policy.

To use our website, you must accept our privacy policy.

Where Swiss asset managers see further potential in 2026

According to a survey of independent asset managers in Switzerland, a clear majority are betting on further price increases for Swiss equities, while other markets are seen as weaker. Investments in domestic real estate are also popular, as is gold.

Swiss asset managers see the greatest opportunities in the SPI, as can be seen from the Aquila Asset Manager Index (AVI) for the fourth quarter of 2025.

When asked which market would offer the most attractive risk/return ratio in 2026, 42% named the Swiss equity index, followed by the emerging markets index (MSCI EM ex China, 18%) and the US blue-chip index S&P 500 (14%). European equities (MSCA EMU, 7 percent), the tech stocks of the Nasdaq 100 and MSCI China (9 percent each) were clearly below expectations. The British FTSE 100 and the Japanese Nikkei 225 were not mentioned at all.

The fear of an AI bubble on the stock market is clearly not too widespread among asset managers. Only 13% of participants expect valuations to "pop". This contrasts with 61% of "semi-optimists", who see a partial overvaluation and expect a slight cooling - but no crash. And as many as 26% continue to see AI as a growth driver and do not yet see the highs being reached.

When asked which investments they would rely on to diversify away AI risk, around 66% named gold. Swiss real estate (36%), cash (32%), infrastructure/energy (29%) and commodities (26%) are also seen by many as a hedge.

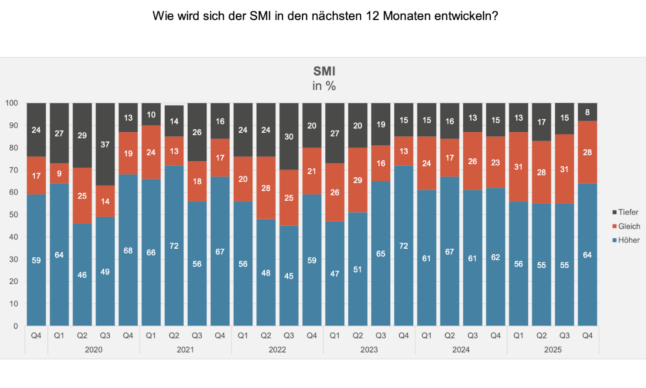

Looking ahead, assessments for the SMI on a 12-month horizon are more optimistic than in the last survey. A rise is now expected by 64 percent instead of 55 percent previously. A stable level is expected by 28 percent and only 8 percent expect prices to fall. The majority of respondents (64%) expect interest rates on 10-year Swiss bonds to remain the same.

(Click on graphic to enlarge)

"Following the recent weakness in November, we slightly increased our equity position and selectively took advantage of attractive investment opportunities," comments Manuela Rupf, Founder and partner of Alpique Swiss Wealth Partners. "We remain optimistic and are focusing primarily on high-quality companies. Bull markets rarely end during periods of interest rate cuts." Broad diversification and a disciplined investment approach remain crucial. "On the client side, we are seeing increased demand for commodity exposure - silver in particular still appears attractive despite the strong movement."

Gold as a central building block

Also Sam Harsch, Chairman of the Board of Directors and Partner at Gotthard Partners, is focusing on precious metals. "Gold has been a central component of our strategic asset allocation for years. The deliberate overweighting at the expense of the bond component is not based on short-term market expectations, but on the assessment that the precious metal will continue to fulfill its function as a store of value and stability instrument in an environment of rising government debt, geopolitical fragmentation and increasing monetary policy uncertainty."

In addition, the exposure of mandates to euro and dollar investments has been reduced for some time. Harsch points to the persistently high level of debt, fiscal conflicts of interest and increasing "monetary policy flexibilization" in the USA and the eurozone. "We assume that, in addition to the US dollar, the euro will also gradually move towards a soft currency."

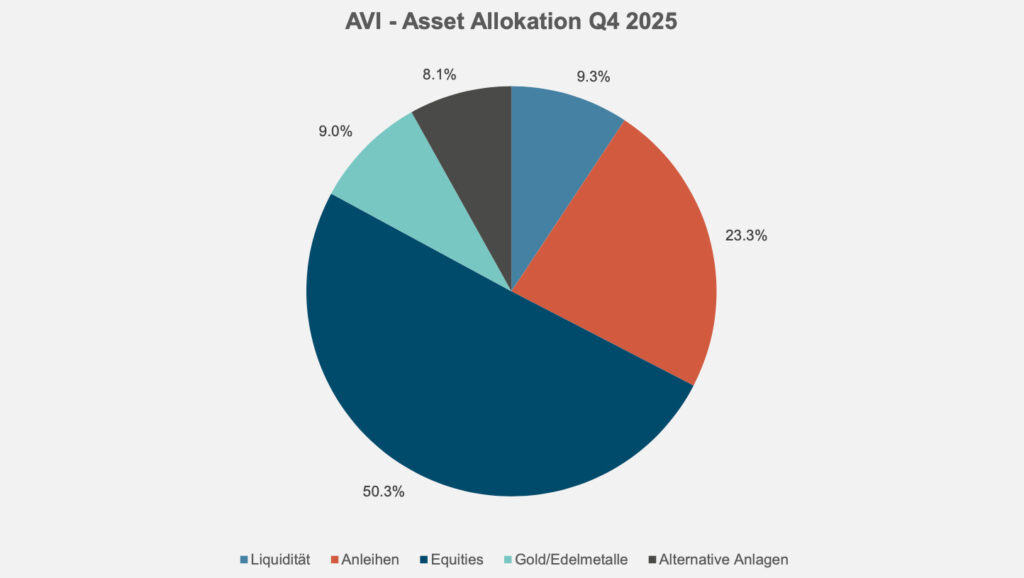

According to the survey, the weighting of equities, liquidity and gold in the asset allocation is clearly above that of a classic balanced portfolio, and below that of bonds.

(Click on graphic to enlarge)

The next AVI Index will be published at the beginning of 2026.

Disclaimer: Produced by Investment Center Aquila Ltd.

Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no under-taking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information pro-vided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other trans

action. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.