This website uses cookies. For more information about this and your rights as a user, please see our Privacy policy.

To use our website, you must accept our privacy policy.

Asset managers consider crypto assets to be overvalued

Independent asset managers in Switzerland are currently facing a difficult market situation. Many assets are proudly valued after the bull market in the current year, while at the same time the geopolitical fragmentation of the world does not make it easy to make the right investment decisions, as the latest edition of the AVI Index shows.

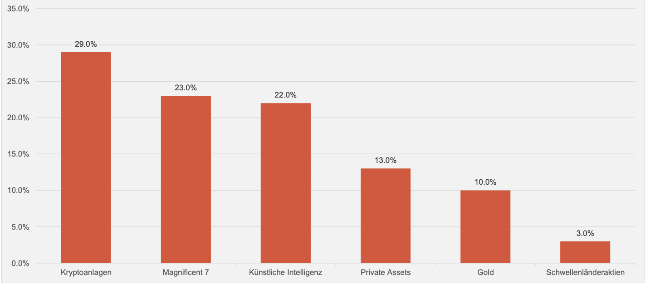

NNow that crypto assets have skyrocketed this year, the euphoria could now recede somewhat. At least that's what independent asset managers in Switzerland think. Almost 30 percent of them are of the opinion that digital assets are currently overvalued, according to the latest AVI-Index (cf. graphic below).

(Click on graphic to enlarge)

The AVI index is published quarterly by the Swiss Aquila Group in cooperation with finews.ch was created. It summarizes various forecasts and assessments by independent asset managers in Switzerland. A total of 150 companies took part in the latest survey.

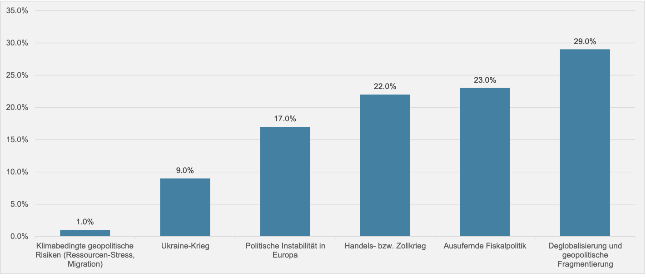

Biggest concern

In connection with the highly diffuse global political developments of recent months, almost 30 percent of the asset managers surveyed cited deglobalization and geopolitical fragmentation as their biggest concerns, followed by excessive fiscal policy in some countries (cf. graphic below).

(Click on graphic to enlarge)

"The economic policy announcements made by US President Donald Trump are increasingly causing uncertainty on the currency markets. Investors have doubts about fiscal sustainability and are pricing political risks directly into the dollar. At the same time, a weak dollar is certainly in the interests of the US President, as it should supposedly support the competitiveness of American exports," says Urban AneggPartner at Brennwald & Partner in Zurich.

"Against this backdrop, we prefer Swiss quality companies with healthy balance sheets and sustainable growth; real compounders that create value even in a challenging environment. In addition, a strategic gold position remains a sensible anchor of stability in politically uncertain times," Anegg continues.

Confident behavior

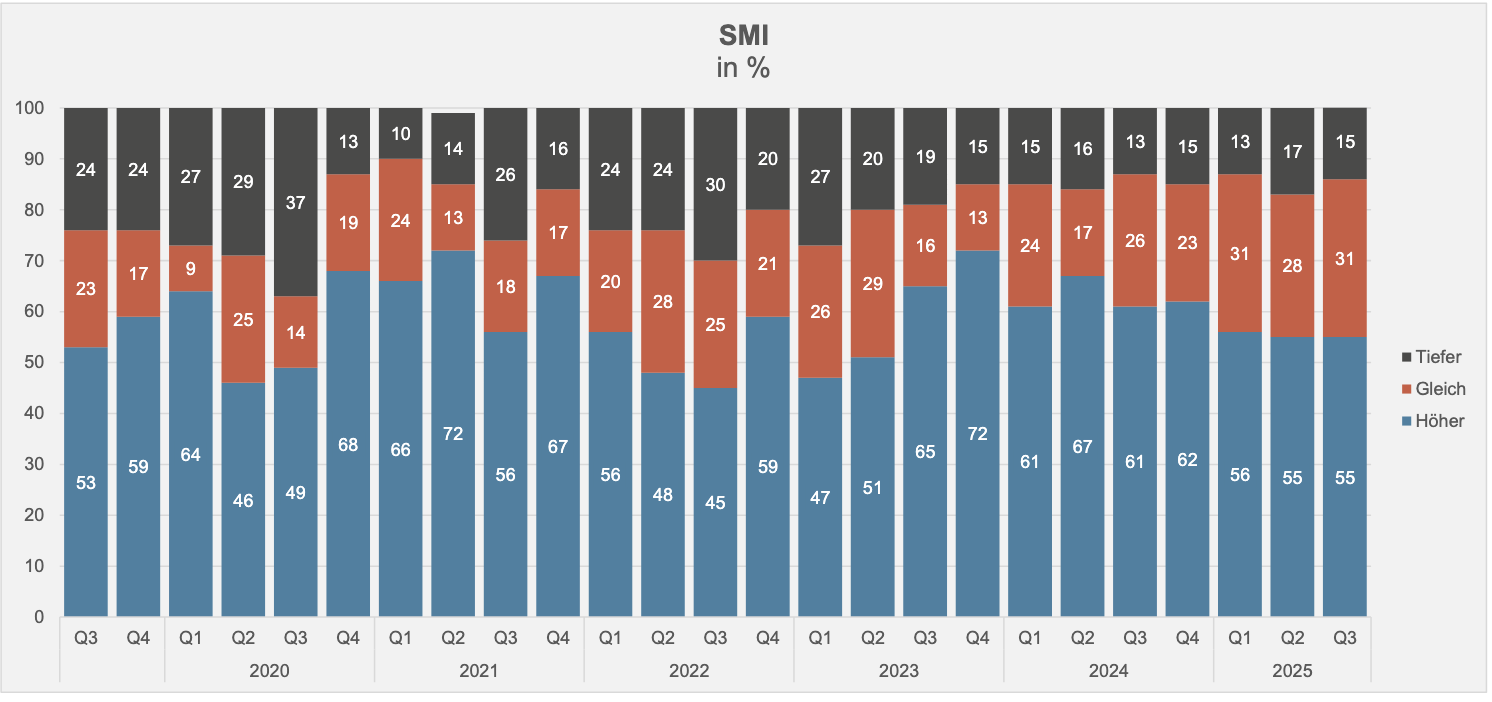

Despite the somewhat gloomier outlook, many asset managers are confident, as the survey also shows. As was the case three months ago, 55 percent of participants expect the Swiss Market Index (SMI) to rise, while 15 percent anticipate lower prices (cf. graphic below). At the middle of the year, the figures were 55% and 17% respectively.

(Click on graphic to enlarge)

No longer coherent

"The gap between the economic slowdown and positive stock market performance is widening. The equity market seems willing to see through the short-term economic challenges, supported by a renewed rise in interest rate cut expectations - despite rising inflation", explains Johannes BornerCIO/Research at Santro Invest in Feusisberg.

"The picture is no longer coherent for us, so it makes sense to reduce the risk in the portfolios somewhat and take some of the good equity performance with us," Borner continues.

Flight into quality values

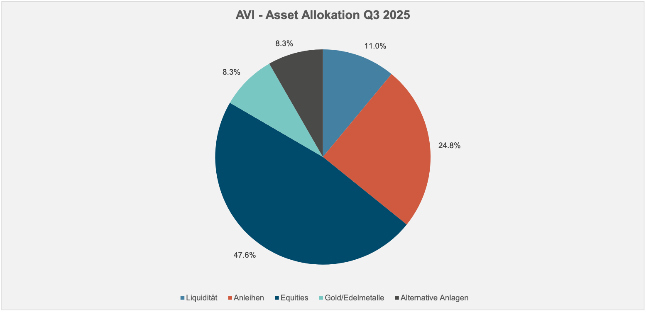

In their asset allocation, independent asset managers have increased their exposure to equities compared to the middle of the year, namely to 47.6 percent compared to 46.2 percent at the end of June 2025.

However, the proportion of bonds has also increased and currently stands at 24.8% compared to 23.8% at the middle of the year. These two changes were at the expense of liquidity, which fell to 11.0% compared to 12.7% at the end of June 2025 (cf. graphic below).

(Click on graphic to enlarge)

In view of the high gold prices in recent months, many independent asset managers have also reduced their positions in the yellow precious metal; they now have a share of 8.3 percent, down from 8.8 percent at mid-year. Alternative investments also fell slightly, from 8.5 percent at mid-year to 8.3 percent.

In fact, many independent asset managers currently appear to be concentrating on quality stocks, primarily of Swiss origin. This also helps to contain currency risks, which must be taken into account, especially as the dollar continues to fall.

The next AVI Index will be published at the beginning of 2026.

Disclaimer: Produced by Investment Center Aquila Ltd.

Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no under-taking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information pro-vided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other trans

action. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.