This website uses cookies. For more information about this and your rights as a user, please see our Privacy policy.

To use our website, you must accept our privacy policy.

Aquila Viewpoints

Market Outlook | 1st Quarter 2023

23 December 2022

Tactical Perspective:

Macro

Bonds

Equities

Other Asset Classes

Executive Summary

Central banks have been raising key interest rates to fight inflation and this will continue in the coming year. They will also reduce the size of their balance sheets.

We expect a dwindling growth momentum which will lead to recession in some countries. Ultimately, this will allow central banks to loosen monetary policy in a measured way in the second half of 2023.

Regarding the market outlook, one of the central questions is whether investor profit expectations for the coming year can be met or whether they will need to be revised downwards.

The inversion of the US yield curve points to a looming recession.

Equities have come under renewed pressure after central banks signal they have further tightening to do.

Regarding the market outlook, one of the central questions is whether investor profit expectations for the coming year can be met or whether they will need to be revised downwards.

The US dollar’s trend rise has come to a standstill and Gold has shown an impressive performance in recent weeks.

Our macroeconomic assessment

Business cycle

Our growth forecasts for 2023 are: World 2.1%, US 0.4%, EU -0.1%, Japan 1.5%, China 4.5%, UK -0.2%, Switzerland 0.6%.

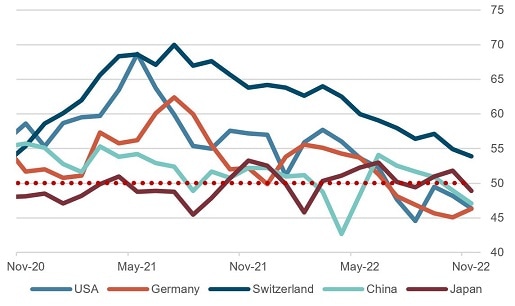

Purchasing managers’ indices and leading indicators are falling, giving a clear and consistent message of an economic slowdown and point to a recession.

Thanks to comparatively low inflation and lower interest rates, Switzerland is in a noticeably better situation than other countries or regions.

In Europe, and especially Germany, the very negative outlook is easing thanks to a rather mild winter so far and the growing likelihood that the feared energy shortage can be averted. Nevertheless, the collapse of numerous indicators, including the ZEW survey indices, argues for a recession.

The labor market in the USA remains tight. Some layoffs are expected from January onwards, given operational problems at the corporate level and fading growth momentum.

The outlook for 2023 is rather uncertain due to the high (geopolitical) risks and the limits to which governments and central banks can control events. Such factors cannot really be predicted.

The US Presidential cycle sheds a positive light on the outlook for 2023 towards the end of the year.

Monetary policy

The high liquidity injections of recent years are at least partly responsible for current high inflation rates. We forecast that central banks will be reducing their balance sheets, albeit at varying speeds depending on the prevailing conditions.

Purchasing managers’ indices, last 2 years

Source: Bloomberg Finance L.P.

In November, US consumer price inflation rates continued to decline. In Europe, too, where the inflation figures are still much higher, we see the first signs of slightly falling trend. The upcoming favorable “base effect” is likely to support further declines. However, the more “sticky“ US inflation components as reported by the Atlanta Fed continue to rise, while the volatile and “flexible” components are now falling sharply.

The strong US dollar had a favorable effect on US inflation up to October. In the meantime, however, this influence has reversed.

Central banks are still committed to their 2% inflation target and will continue to tighten monetary policy. A change of direction, even on a temporary basis, should not be expected.

Our investment policy conclusions

Bonds

At the December FOMC meeting a majority of committee members indicated they see the peak of the current rate hike cycle at between 5% and 5.25%. This is higher than the 4.4% to 4.9% range projected in September.

FOMC member projections also indicate that the key interest rate will have to remain at this elevated level for a longer period, above all to slow down the labor market, which is still “too strong” and could therefore lead to a wage-price spiral.

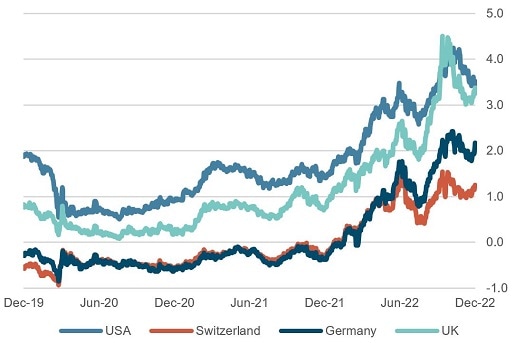

The steadily more pronounced inversion of the US yield curve, which now matches the inversions seen at the beginning of the 1980s, points to an impending severe recession.

In corporate bonds, credit spreads have eased significantly for both good and lower quality issues. This trend, which conveys a different message from the inverted yield curve, could be interpreted as implying: “recession yes, but it won’t be that bad”.

10 year government bond yields in %, last 3 years

Source: Bloomberg Finance L.P.

Equities

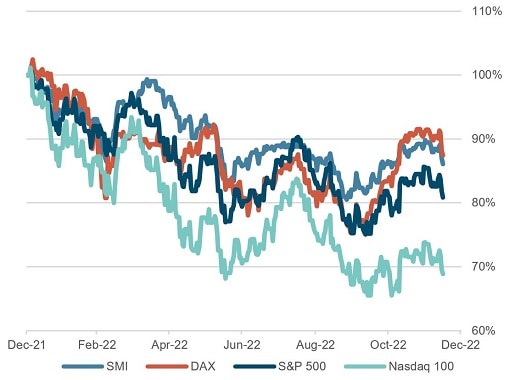

The S&P 500 and Nasdaq indices are still in the downward trend that has existed since the beginning of the year. In this respect, the somewhat friendlier development of the past weeks can be viewed as another “bear market rally”. For European indices, on the other hand, the picture looks somewhat friendlier from a technical perspective.

Factor-related rotations are responsible for some significant differences in the performance of various indices or sectors. For example, “value” stocks have clearly outperformed “growth” stocks in the year to date. This is understandable in a potentially recessionary environment with rising interest rates.

We remain cautious and neutrally positioned in equities. The questions for the coming half-year will probably be whether and to what extent earnings estimates have already priced in a stronger recession than seemed in prospect a few months ago. Particularly in the area of growth stocks, valuations are still quite demanding in some cases and would be vulnerable should a longer recessionary phase occur.

Equity markets, perfomance year to date, indexed

Source: Bloomberg Finance L.P.

Forex

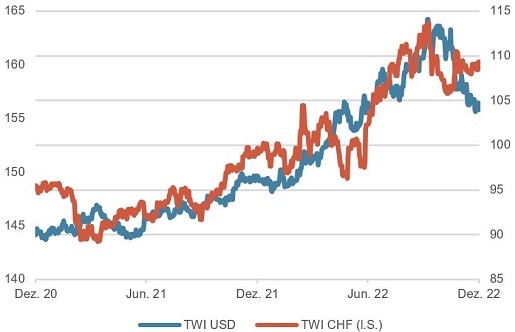

The upswing of the US dollar has come to a standstill. Indeed, the US unit is now around 7% below its 2022 highs against the Swiss franc, with a clear decline against the other main currencies.

Parallel to this, the demand for USD liquidity, which at times increased significantly, has also calmed and corresponding swap prices have receded. This is of great importance for the outlook for all financial markets because high demand for USD liquidity can be equated with high levels of stress in the financial system. We are following this closely.

The weakness of the euro that was evident throughout the summer has recently calmed somewhat. However, Europe’s structural deficits and her unfavorable constellation of geopolitical risks remain.

Dollar and Swiss franc trade-weighted indices, last 2 years

Source: Bloomberg Finance L.P.

Disclaimer: Produced by Investment Center Aquila Ltd.

Information and opinions contained in this document are gathered and derived from sources which we believe to be reliable. However, we can offer no under-taking, representation or guarantee, either expressly or implicitly, as to the reliability, completeness or correctness of these sources and the information pro-vided. All information is provided without any guarantees and without any explicit or tacit warranties. Information and opinions contained in this document are for information purposes only and shall not be construed as an offer, recommendation or solicitation to acquire or dispose of any investment instrument or to engage in any other trans

action. Interested investors are strongly advised to consult with their Investment Adviser prior to taking any investment decision on the basis of this document in order to discuss and take into account their investment goals, financial situation, individual needs and constraints, risk profile and other information. We accept no liability for the accuracy, correctness and completeness of the information and opinions provided. To the extent permitted by law, we exclude all liability for direct, indirect or consequential damages, including loss of profit, arising from the published information.